Main Content

Lesson 1: Introduction to Accounting and Business

Four Types of Business Organizations

Note: This lesson's content uses a slide carousel. Once you have completed the current slide, please click on the subsequent sphere at the top of the carousel to proceed to the next topic.

Sole Proprietorship

A sole proprietorship (also called a single proprietorship) is owned by one person who is personally liable for all the business's debts. About 70% of the businesses in the United States are sole proprietorships. Figure 1.1 shows the relationship between the owner and the business in a sole proprietorship.

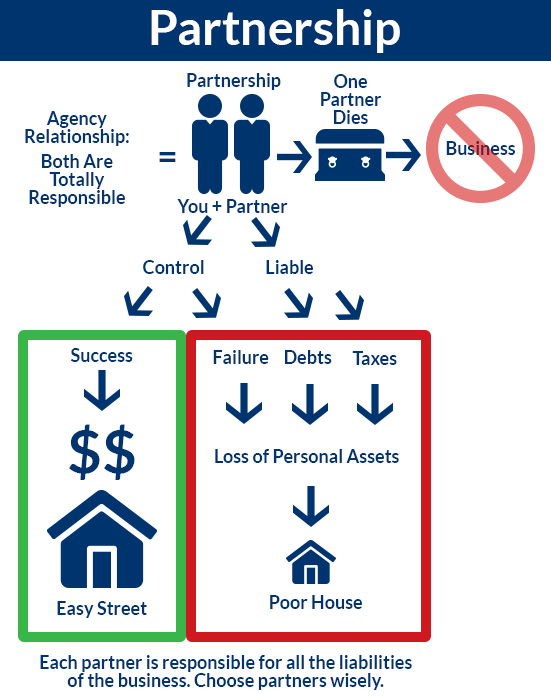

Partnership

A partnership is a business organization that is owned by more than one person. The owners are liable for all the debts of the business. These relationships are reflected in Figure 1.2. About 10% of the businesses in the United States are partnerships.

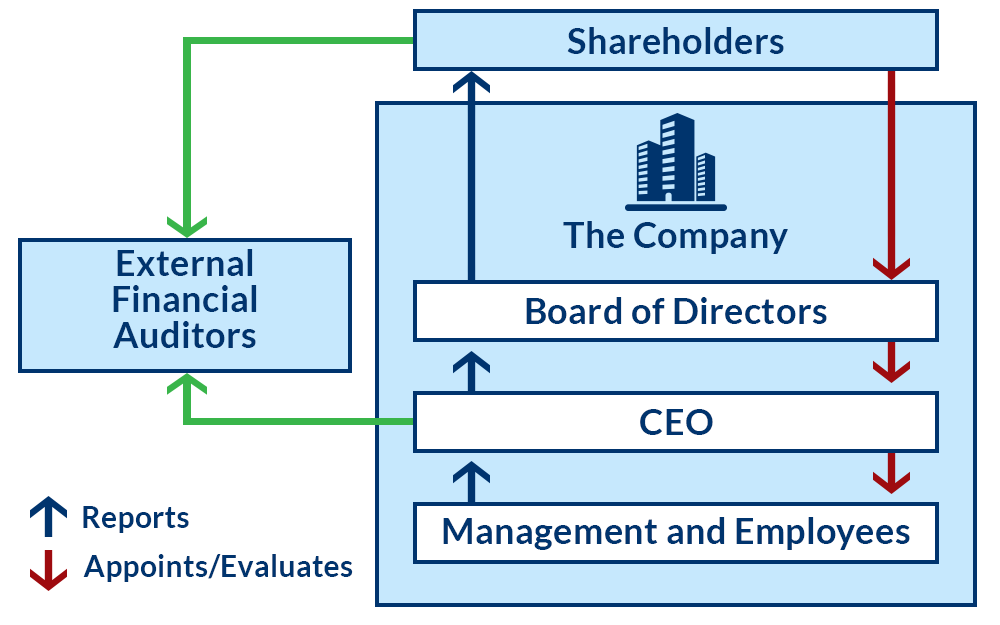

Corporation

A corporation is a separate legal entity in which ownership is divided into shares of stocks. Owners of a corporation are called stockholders or shareholders, because evidence of ownership is expressed with shares of stock. Shareholders are only liable for the amount they invest in the business. Figure 1.3 illustrates the organization of a corporation. About 5% of the businesses in the United State are corporations. However, they are responsible for 62% of the total dollars of business. ( https://taxfoundation.org/corporations-make-5-percent-businesses-earn-62-percent-revenues/ )

All business organizations have their own set of accounting records (separate from their owners). That means that every business transaction that affects the business has to be recorded in the business’s record. The owner may keep his or her own separate set of records.

Example 1.2

The business entity concept states that MM TAX, the tax firm owned by M. McGruber, must keep its financial records separate from McGruber's personal accounts. This means that MM TAX is not purchasing groceries for McGruber and claiming those as a business expense in its records. The business entity is considered to be separate from its owner, even if it is a sole proprietorship, which implies that the owner is the business and the business is the owner. For accounting purposes, the two are considered to be separate.