ACCTG211:

Lesson 1: Introduction to Accounting and Business

Introduction

This course introduces you to the discipline of accounting through an introduction to two of its subdisciplines: financial and managerial accounting. Lessons 1 through 9 cover material in financial accounting. In financial accounting, we generate reports and communicate the information to decision-makers external to the company so that they can evaluate the company. Lessons 10 through 15 cover material in managerial accounting. In managerial accounting, we provide information to internal decision-makers.

Accounting’s role in the decision-making process is key to the course.

We all use basic accounting concepts in our daily lives.Individuals have many of the same transactions that businesses do: we earn money, pay bills, buy assets (such as cars and houses), borrow money, and so on. Businesses record these transactions in their accounting systems and generate reports (financial statements) that summarize the results of operations for a period of time, like a month or year. Businesses are required to follow a set of rules and regulations (generally accepted accounting principles) when they record their transactions and prepare financial statements.

Lesson 1 introduces you to the various concepts and vocabulary necessary for a basic understanding of accounting. The first part of the lesson defines terms that you must know in order to understand the content in the rest of the lessons in the course. The latter part of this lesson focuses on business transactions and their effect on the basic accounting equation, which serves as the foundation for accounting.

Learning Objectives

After completing this lesson, you should be able to do the following things:

-

state the accounting equation and define each element of the equation;

-

demonstrate how business transactions are recorded in terms of changes in the elements of the accounting equation;

-

distinguish among different types of organizations: sole proprietorships, partnerships, corporations, limited liability companies (LLC), and limited liability partnerships (LLP); and

-

describe the four financial statements of a corporation and explain how they are interrelated.

Lesson Readings & Activities

By the end of this lesson, make sure you have completed the readings and activities found in the Lesson 1 Course Schedule.

Business Stakeholders

-

individuals interested in investing in the company by way of purchasing shares and evaluating the return on investments (ROI). We will cover financial ratios in a later lesson.

- managers, who are evaluated according to the performance of the company they manage;

- creditors, who evaluate the company's risk level to determine if lending money is safe;

- the government, which determines if the entity is paying its taxes and/or following set regulations;

- employees, who evaluate their job security and benefits; and

- customers, who evaluate the risk level of products and services.

Watch Video

One of the things that a financial accountant takes into consideration is the stakeholders of a company. Now, a stakeholder is anybody that has an interest in the economic position of that company. And the reason that an accountant cares about the stakeholders, as do the owners of the company, the board of directors, is because these are the people that can influence the success of the company.

For example, when we look at this diagram, you see a spider-web-type situation, and the stakeholders include the following: consumers. Now why would a consumer care about the financial position of a company? Well, if you found out that Ford was going out of business, would you purchase a Ford? Probably not, because you want a company that is going to be around to service your automobile. So therefore, a consumer cares whether the company that they are purchasing from is viable and will be in business.

Suppliers. A supplier cares why? Because obviously, if a company goes under, then they have lost a customer. They are supplying things for this customer, and they want that customer to be successful. They also want the customer to be successful because chances are that customer, that company, owes them money for items that the company purchased from them. So they want to make sure that the company is viable and can pay their bills and will continue to order items from them.

Employees. Obviously, if you're an employee, you want your company to be successful because you want to keep your job.

The local community. The local community cares because if a company is successful, then that means the people in the community have jobs and will have income that they can then spend within that community.

Management. Obviously, management cares for the same reason that employees care. They are managing this company. Their performance has a direct influence on the performance of the company. So if the company is doing poorly, it reflects upon management and they might be out of a job.

Shareholders. A shareholder is another word for an owner. A shareholder is an owner in a corporation. All shareholders are stakeholders, but not all stakeholders are shareholders. So obviously, as an owner, you want your company to be successful.

Government. The government wants a company to be successful, too. Number one, because that company will then pay taxes on whatever incomes the company produces. But more importantly, if that company goes under, the government may have to be paying unemployment or welfare to those employees who no longer have jobs.

So when we talk about stakeholders, just remember that it is someone who has an interest in the success of a company.

Financial and Managerial Accounting

The accounting profession can be divided into different types. The two types that we will discuss in this course are financial and managerial accounting. Others in the profession include analysts, auditors, forensic accountants, consultants, and financial advisors.

Financial accounting provides financial information about the business entity in the form of financial statements to outsiders, such as creditors, stockholders, government agencies, and so on. The financial statements include:

- income statements,

- statements of retained earnings (or statements of stockholders' equity),

- balance sheets, and

- statements of cash flows.

Financial accounting has a defined set of rules and regulations (Generally Accepted Accounting Principles, or GAAP) and an emphasis on the past (historical). We prepare financial statements on a monthly, quarterly, and yearly (annual) basis, in the order listed above.

Internal users (managers) are in need of financial information in their decision-making about the daily operation of the business. The purpose of managerial accounting is mainly to provide financial information about the business in the form of special reports and summaries to managers for internal operational use. Managerial accounting has a future emphasis. We are preparing budgets and the like to help managers in their planning process.

Watch Video

The accounting profession can be divided into several different types of accounting. And the first type that we talk about is financial accounting. Financial accountants provide information to management and to stakeholders about the economic position of the company. They create the historical record, what really happened over the course of the last financial period. It reports the data that are necessary to formulate strategies and policies concerning the operations of the company.

Why do they do this? Well, they do this to enable managers to make decisions about a current business environment. It enables stakeholders to determine their relationship with the company. Do they want to buy shares, sell shares? Do they want to do business with this company? Will they be able to collect any amounts that might be owed them? Would you like to purchase a product or a service from this company?

So the financial records that are created by financial accountants provide the necessary information to make these determinations. It enables a government to determine whether the company's met its legal obligations, to ascertain the economic situations, and it enables competition to evaluate how their industry is doing and to create industry standards.

So when we talk about financial accounting, these are the historians. They analyze each transaction and identify how the transaction actually occurred.

Business Entities

A business entity is an organization that uses resources to provide services or goods to a consumer. The business entity is always treated separately from its owner(s), and each business entity has to have its own set of accounting records. All business entities (organizations) have a significant role to play in society and have multiple stakeholders to whom they are accountable.

Example 1.1

In this lesson we will analyze a transaction for a service company (MM TAX) and show how the results from the transactions are used to prepare the company’s financial statements.

MM TAX is a firm that provides tax services for clients. MM TAX will be organized as a corporation. M. McGruber is the only stockholder of the corporation. M. McGruber uses a computer (resource) to prepare tax returns that are filed by the client with the appropriate taxing authority. MM TAX is a business entity (corporation) that uses resources to provide a service.

Four Types of Business Organizations

Note: This lesson's content uses a slide carousel. Once you have completed the current slide, please click on the subsequent sphere at the top of the carousel to proceed to the next topic.

Sole Proprietorship

A sole proprietorship (also called a single proprietorship) is owned by one person who is personally liable for all the business's debts. About 70% of the businesses in the United States are sole proprietorships. Figure 1.1 shows the relationship between the owner and the business in a sole proprietorship.

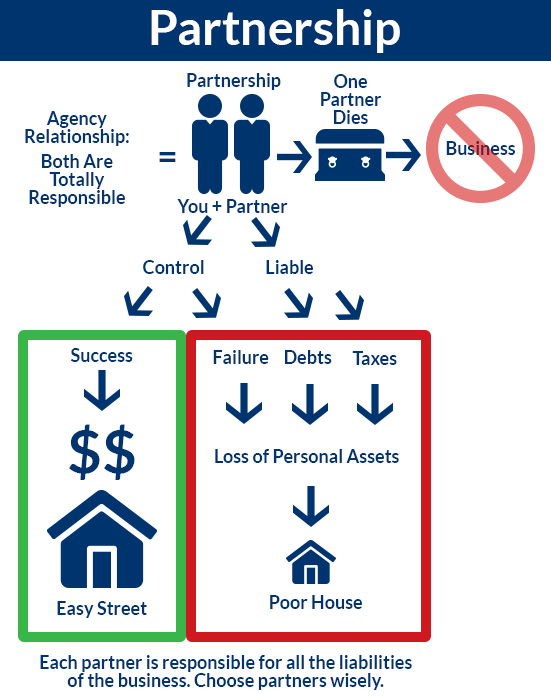

Partnership

A partnership is a business organization that is owned by more than one person. The owners are liable for all the debts of the business. These relationships are reflected in Figure 1.2. About 10% of the businesses in the United States are partnerships.

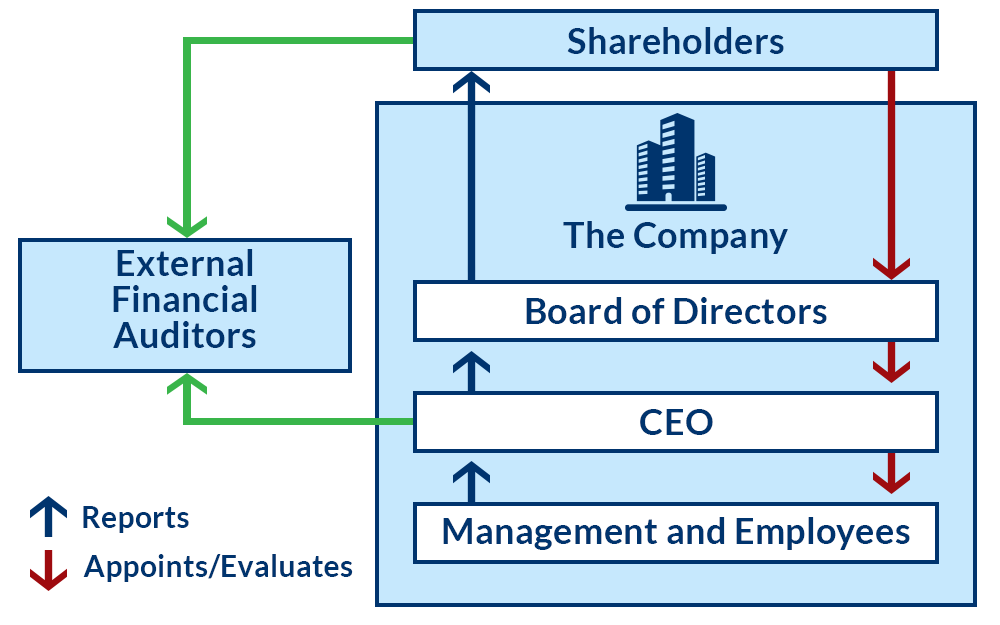

Corporation

A corporation is a separate legal entity in which ownership is divided into shares of stocks. Owners of a corporation are called stockholders or shareholders, because evidence of ownership is expressed with shares of stock. Shareholders are only liable for the amount they invest in the business. Figure 1.3 illustrates the organization of a corporation. About 5% of the businesses in the United State are corporations. However, they are responsible for 62% of the total dollars of business. ( https://taxfoundation.org/corporations-make-5-percent-businesses-earn-62-percent-revenues/ )

All business organizations have their own set of accounting records (separate from their owners). That means that every business transaction that affects the business has to be recorded in the business’s record. The owner may keep his or her own separate set of records.

Example 1.2

The business entity concept states that MM TAX, the tax firm owned by M. McGruber, must keep its financial records separate from McGruber's personal accounts. This means that MM TAX is not purchasing groceries for McGruber and claiming those as a business expense in its records. The business entity is considered to be separate from its owner, even if it is a sole proprietorship, which implies that the owner is the business and the business is the owner. For accounting purposes, the two are considered to be separate.

Generally Accepted Accounting Principles (GAAP)

The generally accepted accounting principles (GAAP) are a set of accounting principles that accountants follow in the process of recording, summarizing, reporting, and interpreting business transactions so that the information provided through the accounting system is consistent from one practitioner to another. The following groups have been responsible for improving accounting principles and practices in the United States: the Financial Accounting Standards Board (FASB), the Securities and Exchange Commission (SEC), the American Institute of Certified Public Accountants (AICPA), and the American Accounting Association (AAA).

Listen to the following audio clip.

When we talk about the rules of accounting, we talk about generally accepted accounting principles, otherwise known as GAAP. These are the rules that we play by. Just as when you decide you want to play a game, and everybody wants to be on the same page and wants to know what the rules are, all accountants should follow the same rules so that when we look at financial statements, or we look at historical documents regarding the financial position of a company, we know what they really mean. We're all playing by the same standards.

Consider that you may call one of your friends and say, "Let's get together and play some football." And you gather a group of people. And you arrive at the field in your American football regalia only to be met by another group of people who are dressed to play English football, or soccer. Obviously, you're following two different sets of rules and you're not going to be successful at either one.

GAAP are the rules, the generally accepted accounting principles. And these are created by several different groups that are responsible for improving those principles, or for creating the principles. FASB, the Financial Accounting Standards Board; the SEC, the Security and Exchange Commission; the AICPA, the American Institute of Certified Public Accountants; and the AAA, the American Accounting Association. Each of these groups has input into creating the rules that we follow, and it's very important that we follow these rules.

And throughout this course you will be hearing about different principles, and policies, and standards. And each one of these follows GAAP. So to explain what GAAP is, these are the generally accepted accounting principles that everybody plays by in the United States.

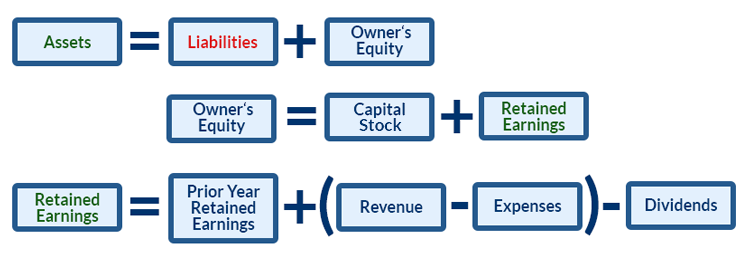

The Basic Accounting Equation

- assets, or what the company owns or has rights to;

- liabilities, or what the company owes; and

- owner’s equity (abbreviated OE and also known as stockholders' equity).

The basic accounting equation, shown in Figure 1.4, shows the relationship among these elements.

Essential Concepts

It is essential that you have a good grasp of the concepts in Figure 1.5 in order to progress smoothly in accounting studies. These terms will be explained in more detail and with examples in the next few pages. They form the basis of financial statements and are essential for properly analyzing transactions. Please spend enough time to master them.

Assets: Items Owned by the Company or to Which the Company Has Rights

An asset is an economic resource owned by the business; it is expected to be used to benefit the operations of the business and generate revenue.

Examples include

- cash,*

- accounts receivable,**

- supplies,

- merchandise inventory (introduced in Lesson 5),

- automobiles,

- equipment,

- buildings, and

- land.

An asset also includes anything that will add future value to your business.

Example 1.4

MM TAX purchases paper needed to complete tax returns for its clients. This paper is an asset because it generates income. MM TAX also uses a computer to calculate the tax returns that are created for the tax clients, so the computer is an asset. Equipment used in the generation of revenue is an asset.

Liabilities: What the Company Owes

Liabilities are the business's debts (i.e., creditors' claims on assets). Either borrowing money or buying on credit creates a liability.

Examples include

- accounts payable,

- notes payable,

- taxes payable,

- utilities payable, and

- wages payable.

We will discuss accounts payable and notes payable below. Taxes payable refers to the amount owed but not yet paid for taxes. Utilities payable refers to the amount that is owed but not yet paid; we have received the bill but have not paid it yet. Wages payable represents the amount of wages due to employees that have not yet been paid. Lesson 3 will explain wages payable in greater detail.

Accounts Payable (A/P)

Accounts payable (A/P) refers to our promise to pay in the future for services performed for us or for goods purchased.

Notes Payable (N/P)

A note payable (N/P) occurs when the debt will not be paid in a short period of time (usually 30 days), and therefore the creditor (the person you owe) will expect additional compensation in the form of interest for the use of her money. The note usually includes a written promise to pay and contains terms concerning the due date and interest rate.

Think in terms of your own experiences: You borrow money from a bank to purchase a new car. The bank loans you the money for three years at an annual interest rate of 6%. You have a note payable. You will make monthly payments to repay the loan. Your monthly payments include payment toward the principal (repaying the amount owed) and interest (your cost to borrow money).

Liability Due to Prepayment

Another type of liability occurs when the company has received a prepayment for products or services that have not yet been delivered. The company now has a liability because it owes something: It must deliver on the product or service or it must return the money.

Stockholders' Equity (aka Shareholders' Equity or Owners' Equity)

Stockholders' equity represents the owners' investment in the business (i.e., the owners' claim on assets). The term owner’s equity (OE) applies to all the business formats (sole proprietorship, partnership, and corporation), but the term stockholders' equity refers only to the owners of corporations, because those who own shares of stock in a corporation are the owners of that corporation.

Stockholders' equity has the following components:

- capital stock or common stock: If the business issues shares of stock (i.e., ownership) to investors in exchange for $100,000, the $100,000 that has to be paid by the investors to purchase the stock is called capital (or common) stock. Capital stock is recorded at the initial selling price of the stock, and there are no adjustments for increases and decreases in market value.

- retained earnings: This represents earnings reinvested in the business rather than distributed to owners as dividends. For example, if the business makes $120,000 profit and distributes $40,000 of this to owners as dividends, retained earnings (owners' equity) in the business would go up by $80,000.

- dividends: Dividends are distributions of cash or other assets to the stockholders. Note that dividends do not appear on the balance sheet. They are closed to retained earnings before the balance sheet is prepared (explained in Lesson 4).

The following are also included in stockholders’ equity in Lesson 1:

- revenue: Revenue is the amount earned from delivering services or goods to customers. Revenue is initially included in equity.

Examples include- fees earned,

- service revenue,

- commissions earned, and

- sales revenue (explained in Lesson 5).

- expenses: An expense is a normal cost incurred in the selling of goods or services.

Examples include- wages expense,

- utilities expense, and

- advertising expense.

Cash Versus Accrual Basis of Accounting

There are two different timings that are used in accounting to record revenues and expenses: cash basis and accrual basis. When to recognize (or realize) revenue depends on which accounting basis is used by the business. The first accounting basis we will discuss is cash basis of accounting. The difference between the cash basis and accrual basis of accounting is discussed in detail in Lesson 3. It is included here because we use the accrual basis of accounting beginning in Lesson 1.

Cash Basis of Accounting

The cash basis records revenues for the period in which cash is received for the goods sold or services rendered, and records expenses for the period in which cash is paid for the goods and services used. Therefore, cash has to change hands for a business to realize revenue and/or expenses. The cash basis is used by individuals and some small businesses.

Accrual Basis of Accounting

All transactions in this course will be recorded using the accrual basis of accounting.

The accrual basis records revenues for the period in which they are earned and records expenses for the period in which they are incurred, without regard to whether cash has been received or paid. Revenues are realized when the goods are sold or services rendered (or both), and expenses are recognized when the goods or services (or both), are used up, not when the cash changes hands between the parties. We will be recording transactions using the accrual basis of accounting.

When Are Revenues and Expenses Recorded?

Revenues are recorded when earned, not necessarily when the cash is received.

Expenses are recorded when they are incurred, not when the company paid for them.

Example 1.8

Accounting Transactions and Their Effects on Business

A transaction is a business event that can be measured in terms of money. It is an event that impacts an entity's financial position or affects its operations. Very simply, this could mean paying the light bill, purchasing equipment, or shutting down a factory.

Below, we will analyze and record the transactions for MM TAX for December and later use the results to complete the financial statements.

Remember, assets must equal liabilities plus owner’s equity.

Financial Statements

Financial statements are reports that are prepared based on recorded and summarized transactions. Financial statements are used by decision-makers to determine the performance and financial condition of a business. There are four basic financial statements:

- The income statement is a document that shows a company's revenues and expenses during a stated time period. It is sometimes called a statement of earnings.

- The statement of retained earnings is a document that indicates the accumulation of profits that have been "retained" by, or reinvested in, the company.

- The balance sheet is a document that shows the financial position of the company at one moment in time. It is depicted in terms of the accounting equation accounts (assets, liabilities, and owners' equity).

- The statement of cash flows is a document that shows the sources (inflows) of cash receipts and the uses (outflows) of cash payments for the company during a stated time period. This statement will be discussed in later lessons as an indicator of the solvency of a company.

Income Statement

An income statement measures the performance of the business by summarizing revenues and expenses for a given time period (that is, the accounting period). The accounting period, for example, might be a month, a quarter, or a year. Basically, net income or loss may be expressed as in Figure 1.6.

It is very important to know when revenue is generated and expenses are incurred so that proper income is determined for a given accounting period. Make sure you understand the following definitions of revenue and expense:

- Revenue is the amount that is earned from goods sold and services rendered in a given time period. To generate revenue, either goods need to be sold or services need to be rendered (or both). If none of these occur, then there is no revenue.

- Expenses refer to the cost of goods and services used up in the process of generating revenue in a given time period. To incur revenue, either goods or services (or both) need to be used up. An expense is the use of an asset (cash, equipment, or supplies).

Example 1.9

We will use the balances in the accounts of MM TAX at the end of business on December 31 to prepare the financial statements. The first statement we prepare is the income statement.

After all of the transactions are recorded, MM TAX has the following accounts with balances:

| Assets: | Liabilities: | Owner's equity |

|---|---|---|

| Cash $19,100 | Accounts payable $50 | Common stock +$20,000 |

| Accounts receivable $2,500 |

-

|

Dividends -$200 |

| Office supplies $50 |

-

|

Fees earned +$2,500 |

| Computer +500 |

-

|

Salary expense -$200 |

| Total assets $22,150 | Total liabilities $50 | Total owner's equity $22,100 |

The income statement is prepared as follows:

Fees earned is the revenue account for MM TAX, and salary expense is the only expense account for the company. The income statement for MM TAX is shown below:

| Fees earned |

-

|

$2,500 |

|---|---|---|

| Expenses: |

-

|

-

|

|

Salary expense

|

$200 |

-

|

| Total expenses |

-

|

$200 |

| Net income |

-

|

$2,300 |

* Net income will carry forward to the statement of retained earnings.

Statement of Retained Earnings

A statement of retained earnings shows the summary of changes in profits reinvested in the business instead of distributed to owners as dividends in a given time period (for example, a month, a quarter, or a year). Retained earnings is determined as follows:

beginning retained earnings (the amount of profits left in the business at the end of the last period)

+ net income (revenue minus expenses amount from the current income statement)

- net loss (revenues minus expenses amount from the current income statement)

- dividends (profits paid to owners)

ending retained earnings

Let's examine what this really means. If this is the first period of operations, there will not be any beginning retained earnings. If the company has been in business and has left prior period earnings in the company (not distributed to owners), then that is the starting place. To that we add any current period profits, which are determined using the income statement (revenues minus expenses). However, if any profits are distributed to owners (dividends), those profits must be subtracted, because that amount is not being "retained" in the company. The result is the retained earnings that will become part of the owner’s equity.

Example 1.10

MM TAX started business in December 20XX. On December 31, MM TAX is completing its financial statements. Using the income statement that was just completed, we can complete the statement of retained earnings. MM TAX has a beginning balance of $0 and a net income of $2,300 from the income statement. MM TAX also paid $200 in dividends during the period.

The statement of retained earnings for MM TAX is shown below:

| Beginning retained earnings |

-

| $0 |

|---|---|---|

| Add: net income for month | +$2,300 |

-

|

| Less: dividends | -$200 |

-

|

| Increase in retained earnings |

-

| $2,100 |

| Ending retained earnings* |

-

| $2,100 |

The Balance Sheet

The balance sheet measures the financial strength of a business at a particular date by comparing assets, liabilities, and stockholders' equity. Essentially, the balance sheet represents the basic accounting equation. The balance sheet is a snapshot of the company's financial position. It is only accurate for a moment in time because it reflects what the company currently owns and owes, as well as the claims of the owners. As soon as the company completes a transaction, the balance sheet will change to reflect the effects of that transaction.

The balance sheet, which illustrates the different components of the accounting equation, is completed after the income statement and statement of retained earnings are calculated. The items from those statements become part of the balance sheet as a component of owners' equity.

Example 1.11

MM TAX has the following account balances for December 20XX, which appear on the balance sheet:

- assets: cash, $19,100; accounts receivable, $2,500; office supplies, $50; and computer, $500

- liabilities: accounts payable, $50

- owner's equity: common stock, $20,000

In addition, the retained earnings of $2,100 from the statement of retained earnings is included in the balance sheet.

The following accounts do not appear on the balance sheet:

- dividends, -$200 (statement of retained earnings);

- fees earned, +$2,500; and

- salary expense, -$200 (income statement).

| Assets | Liabilities | |||

|---|---|---|---|---|

| Cash | $19,100 | Accounts payable | $50 | |

| Accounts receivable | 2,500 | Stockholders' Equity | ||

| Office supplies | 50 | Common Stock | $20,000 | - |

|

Computer

|

500

|

Retained Earnings

|

2,100

|

-

|

|

-

|

-

|

Total Stockholders' Equity |

-

|

22,100 |

| Total Assets |

$22,150 |

Total Liabilities & Stockholders' Equity |

-

|

$22,150 |

Notice that the balance sheet is a snapshot of the financial position of the company. It is only true for one moment in time because as soon as the company completes a transaction, the account balances will change.

Notice that the balance sheet is the depiction of the accounting equation.

The Statement of Cash Flows

This financial statement demonstrates the receipt and use of cash during an accounting period. This statement will be studied in depth in later lessons.

Practice Problems

Problem 1

Determine the effects of the following transactions on the accounting equation:

-

Issued 20,000 shares of common stock in exchange for $100,000 worth of land.

-

Purchased office supplies for cash for $800.

-

Purchased for $15,000 a car to be used in business. Paid $5,000 in cash and signed a note payable, promising to pay next year.

-

Purchased office equipment on credit for $2,000.

-

Paid $2,400 for employee wages.

-

Rendered services to clients on credit for $18,000.

-

Rendered services to clients and received cash for $42,000.

Click here to find out the answer to Problem 1.

Problem 2

Use the following account balances for the month of May, ending May 31, and determine the following:

-

the net income for May,

-

the statement of retained earnings as of May 31, and

-

the total assets, liabilities, and stockholders' equity as of May 31.

| Assets | Account balances | Liabilities and stockholders' equity | Account balances |

|---|---|---|---|

| Cash | $15,000 | Building | $120,000 |

| Accounts receivable (A/R) | $4,000 | Accounts payable (A/P) | $60,000 |

| Supplies | $3,000 | Salaries payable | $1,000 |

| Equipment | $30,000 | Interest payable | $10,000 |

| Land | $5,000 | Capital stock | $51,500 |

| Dividends | $26,000 | Utilities expense | $1,000 |

| Fees earned | $85,000 | Supplies expense | $500 |

| Salary expense | $15,000 | Retained earnings, May 1 | $14,000 |

| Advertising expense | $2,000 |

-

|

-

|

| Retained earnings (balance as of May 31) | = Retained earnings (balance as of May 1) |

|

-

| + net income |

|

-

|

net loss

|

|

-

|

dividends

|

| Retained earnings (balance as of May 31) | = $14,000 + $66,500 - $26,000 |

|

-

| = $54,500 |

| Total assets | = cash + A/R + supplies + equipment + land + building |

| = $15,000 + $4,000 + $3,000 + $30,000 + $5,000 + $120,000 | |

| = $177,000 |

| Total liabilities | = A/P + salaries payable + interest payable |

| = $60,000 + $1,000 + $10,000 | |

| = $71,000 |

| Total stockholders' equity | = capital stock + retained earnings |

| = $51,500 + $54,500 | |

| = $106,000 |