After completing this lesson, you should be able to

By the end of this lesson, make sure you have completed the readings and activities found in the Lesson 1 Course Schedule.

Individuals, businesses, and government agencies care about taxes for a variety of reasons.

Understanding taxes can help individuals (you!) make informed decisions in many daily aspects of life. For example,

Businesses may also make several decisions based upon the tax consequences; therefore, it is important for them to understand how taxation may affect

Government agencies implement tax systems. When setting these systems in place or when making changes, legislators must consider who, what, when, where, why, and how much to tax. Additionally, they need to consider how the tax may affect political candidacy.

Taxes are the price we pay for civilized society.

The three main characteristics that all taxes share is that they are mandatory, imposed by the government, and not directly linked to a specific taxpayer benefit.

These are required by law and are not voluntarily paid.

Governments (federal, state, and local) impose taxes to raise revenue for operations and programs that they provide.

Taxes paid by the taxpayer have no direct link to any particular benefit received by the taxpayer. For example, taxpayers will receive the benefits of national defense by our federal government regardless of their payment of taxes. Table 1.1 shows examples of tax programs by governmental level.

| Governmental Level | Programs Taxes Pay For |

|---|---|

| Federal |

National defense Judicial system Social programs

Interstate highways |

| State |

Law enforcement Public schools Low-income assistance Unemployment Environmental programs Road maintenance |

| Local |

Police and fire departments Education Libraries Special projects |

The U.S. Constitution (Article I, Section 9), as originally written, actually prohibits an income tax. It says, "No Capitation, or other direct, Tax shall be laid unless in Proportion to the Census" (U.S. Const. art. I, § 9). In other words, taxes were to be in proportion to the population, not income. So, if New York had 10% of the population, their citizens should pay 10% of the taxes. Despite this prohibition, Congress did impose an income tax.

Please scroll through Figure 1.1 below to view a timeline of the history of income tax in the United States.

There are many different types of taxes levied at the federal, state, and local levels.

There are six federal, state, and local individual taxes, and there are five federal, state, and local business taxes. Table 1.3 is blank. Please attempt to complete the table on your own by identifying all of the federal, state, and local taxes you can think of for both individuals and businesses.

| Individual | Business |

|---|---|

The following are characteristics of a “good” tax (from Adam Smith’s Wealth of Nations, published in 1776).

Taxpayers should know when a tax will be imposed, how it will be imposed, and the amount of the tax.

It should be easy (convenient) for taxpayers to pay taxes. Convenience is the argument given for income and employment taxes being withheld from taxpayers’ paychecks and for quarterly estimated payments of taxes when needed. Paying in these ways is more convenient for the taxpayer than waiting until the annual tax return is completed and paying the entire amount of taxes at one time.

Based on Adam Smith's model of economics, the costs of administration of a tax system should be minimal and efficient for both the tax collecting agency (IRS) and the taxpayer. In other words, a tax system should not cost a lot of money to implement, collect, or enforce tax laws for either the IRS or the taxpayer, and it should be easy for the taxpayer to understand and pay taxes owed.

A tax should be based on a taxpayer’s ability to pay. This is usually an income-based decision, though other factors can apply. These equality considerations are captured in two concepts—horizontal equity and vertical equity.

Taxpayers who are situated similarly should pay similar taxes. For example, if we look at two households that are next-door neighbors, and each consists of a married couple with two children and similar household incomes, then those two households should pay a similar amount of taxes. If that is the case (i.e., the two households pay a similar amount of taxes), then there is horizontal equity. If it does not hold true (i.e., they pay dissimilar amounts of taxes), then there is horizontal inequity.

Taxpayers who are not situated similarly should not pay similar taxes. For example, if we look at two households that are next-door neighbors, and each consists of a married couple with two children, but one household earns $200,000 per year while the other household earns $100,000 per year, then the household with the higher income should pay more taxes than the lower income household (ideally twice as much, based on the amounts of income). If that is the case (i.e., that the higher earning household pays about twice as much in taxes), then there is vertical equity. If it does not hold true, then there is vertical inequity.

You will often hear politicians and policymakers describe taxes as progressive, proportional, or regressive, which describe the vertical equity of a tax.

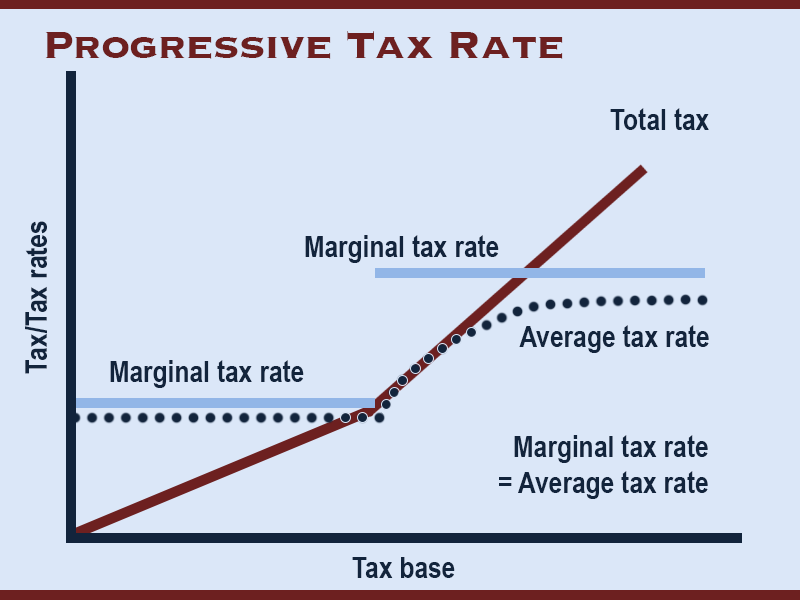

A progressive tax (Figure 1.2) is one in which higher income taxpayers pay a higher percentage of their income than do lower income taxpayers. This is the justification used for our current individual income tax rates, which (for 2023) start at 10% for the lowest income taxpayers and rise to 37% for the highest income taxpayers.

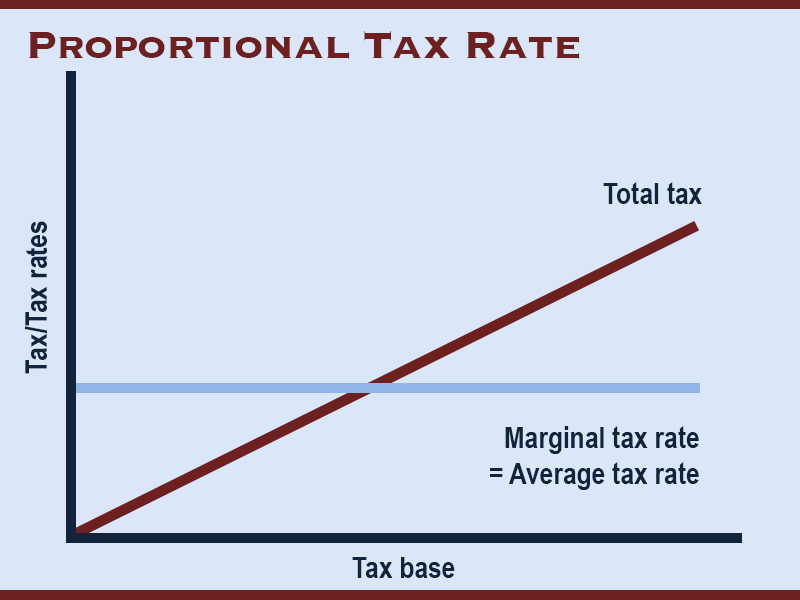

A proportional tax (Figure 1.3) is one in which higher income taxpayers pay the same percentage of their income as lower income taxpayers. Some examples of this are the corporate tax rate (21% in 2023) and sales tax.

A regressive tax (Figure 1.4) is one in which higher income taxpayers pay a lower percentage of their income than do lower income taxpayers. An example of this is the social security tax, which is only imposed on earned incomes up to $160,200 (the 2023 amount). Any earnings above that amount pay zero social security tax, and interest and dividends, which are mostly earned by higher income taxpayers, are not subject to this tax.

Those who implement the tax systems, as well as taxpayers, often use criteria to evaluate the system.

Sufficiency refers to if the tax system is actually generating the amount of revenue that it was expected or budgeted to. Although revenues and expenditures of the government can be difficult to estimate, it is important that the revenue is generated to continue to fund the programs. Although governments do their best to predict this, some unforeseen circumstances, such as wars, natural disasters, pandemics, and economic events can greatly affect the amount of revenue generated by taxes or the expenditures needed to aid in these events.

There are two approaches to forecasting—static or dynamic.

It is difficult to predict a taxpayer’s reaction to tax increases as it will depend on each individual’s preferences. Forecasters and legislators will assume either an income effect or a substitution effect.

When implementing a tax system, there is generally a trade-off between simplicity and fairness. Tax systems that have ease of administration (for example, flat rate tax) generally are most criticized for fairness (not based on ability to pay). The systems that are more complex to administer (for example, graduated tax) are generally seen as most fair by taxpayers. The implementing agencies must determine which they are willing to compromise based on their resources available.

Please review and learn about the IRAC method and bluebooking for use in both your online discussions and your memos. Where applicable, students need to substantiate their thoughts or opinions in the online discussions in lieu of just a general opinion or thought without something to substantiate it. Below you will find references and sites that illustrate how to accomplish these two objectives.

The IRAC method is the standard in the business world as far as discussions in memorandums and should be used as a basis for your online discussion. Read How to Brief a Case Using the "IRAC" Method and watch the following videos for details on this method.

Bluebooking is the preferred method for citing memorandums and should also be used as a basis for your online discussions.

In this lesson, we were introduced to the concept of taxation including what qualifies as a tax, the history of taxation, and types of taxes. We also were able to practice calculating marginal, average, and effective tax rates. Finally, we analyzed how to evaluate tax systems.

Compania General de Tabacos de Filipinas v. Collector of Internal, 275 U.S. 87 (1927). http://caselaw.lp.findlaw.com/cgi-bin/getcase.pl?court=us&vol=275&invol=87

U.S. Const. art. I, § 9.