ACCTG404:

Lesson 1: Course Orientation and Defining Managerial Accounting

Introduction

Hemara/Thinkstock

Managerial accounting is a type of accounting that greatly differs from the financial accounting branch you have studied thus far. In this lesson, you will start to learn about managerial accounting, and how financial and managerial accounting differ. From there, you will learn how to define costs and about how they are assigned to products in managerial accounting. Finally, you will explore how income statements are produced for a manufacturing organization.

Learning Objectives

After completing this module, you should be able to

- define managerial accounting;

- explain the differences between managerial and financial accounting;

- define the costs involved in manufacturing and how to assign costs to individual products;

- explain the various components of manufacturing costs; and

- prepare income statements for a manufacturing company.

Lesson Readings & Activities

By the end of this lesson, make sure you have completed the readings and activities found in the Lesson 1 Course Schedule.

Managerial Accounting Defined

Managerial accounting is a type of accounting typically only seen and used by those who work within a company. It is also typically forward looking and relies heavily on estimates. Employees use managerial accounting for a number of different reasons, but all fall into one of three categories:

- Planning

- Controlling

- Decision Making

Navigate through the slides below to see how managerial accounting is used during the planning, controlling, and decision making processes.

Planning

The planning aspect of managerial accounting is the process of setting objectives or desired outcomes for a particular period (such as a month, a quarter, a year, or even longer). This can come in the form of setting sales goals, identifying potential cost saving techniques to be implemented, or anything in between that helps a company maximize profit.

Controlling

Controlling is the process of ensuring that the ideas produced in the planning stage have been or are being implemented, and that they are effective. Controlling can be both financial and nonfinancial. Obvious financial controlling is ensuring sales are rising or costs are being reduced. Nonfinancial objectives can be things like lack of machine or employee downtime, increases in company morale; the list is endless.

Decision Making

Decision making is the process of choosing between two or more alternatives. This process cannot be done without planning or controlling, and the opposite can be said as well. The decision-making process can only be done after planning and controlling efforts have been made. If these processes are not done, managers do not have the information necessary to make the best decisions. Alternatively, managers must make choices (decision making) just to implement any planning ideas.

Differences Between Financial and Managerial Accounting

Financial and managerial accounting differ in many ways. Probably the most glaring difference is how the two are governed. As you know, financial accounting is governed by Generally Accepted Accounting Principles (GAAP). This is necessary because of who uses the information: business stakeholders, investors, debtors, government agencies, suppliers and many more.

Managerial accounting, however, is not governed by GAAP or any other specific governing rules. This is possible because company employees are the only ones using the information, so there is no need to make all companies' information look the same. Each company is free to produce managerial accounting information that best suits its needs. However, you will find that most companies produce very similar information, and that is what will be covered in this course: best practices.

The major differences between financial and managerial accounting are shown in Figure 1.1.

| Financial Accounting | Managerial Accounting |

|---|---|

| External users | Internal users |

| Governed by GAAP | Not governed by GAAP |

| Historical information | Forward looking |

| Uses estimates only when necessary | Relies heavily on estimates |

Costs

Much of what we will discuss early in this course will revolve around cost. Watch the video below to learn about determining costs and cost objects.

Video 1.1. Defining Costs (Time: 01:26)

For merchandising companies, determining the costs of the product, or Cost of Goods Sold (COGS), is fairly simple. If a company purchases a product for $100 and resells it for $200, the cost is $100 to the company. But what about manufacturing companies? Of course part of the cost is the amount the company pays for materials within the product, such as lumber for a desk or leather for a desk chair. But what about the costs of paying those assembling the product, and the cost to run the machine, and the utilities of the factory?

We will spend much of the early part of this course assigning costs to cost objects. Cost objects are simply any items for which costs need to be assigned. This can be as simple as how much an individual product costs to produce, or as complex as how much a department costs to run.

Product and Period Costs

Manufacturing companies have two very broad categories of costs: product and period costs.

Product Costs

Product costs are those costs required to be incurred in order to produce a product to be sold. Product costs will fit into one of three categories. Click on the tabs below to read more details about each category.

Period Costs

The other costs manufacturing companies incur are period costs. These costs have nothing to do with the manufacturing of the actual product. This will include things like accounting, sales, utilities of an office building, etc. These costs are certainly needed to become a profitable company, but they are not needed to actually produce the product. Because they have nothing to do with the product, period costs are expensed as incurred, as opposed to entering an inventory and ultimately as COGS.

Self-Check

Determining Cost of Goods Sold

The income statements for merchandising and manufacturing companies, shown in Figure 1.2, are the same.

The difference, however, is determining the cost of goods sold (COGS). In a merchandising company it is what the company pays its suppliers for the merchandise. In a manufacturing company, calculating COGS is a little more difficult and involves a number of steps.

| Net Sales Gross Profit |

| Gross Profit Net Income |

COGS Guided Example

| Beginning Direct Materials Inventory | $ 450,000 |

| Ending Direct Materials Inventory | $ 420,000 |

| Direct Materials Purchases | $ 750,000 |

| Beginning Work in Process Inventory | $ 200,000 |

| Ending Work in Process Inventory | $ 300,000 |

| Direct Labor | $ 300,000 |

| Factory Overhead | $ 150,000 |

| Beginning Finished Goods Inventory | $ 400,000 |

| Ending Finished Goods Inventory | $ 350,000 |

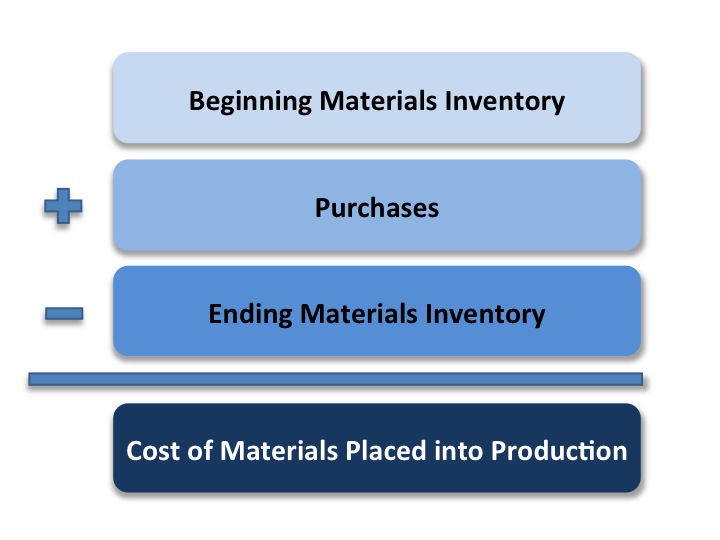

Step 1: Cost of Materials Placed into Production

The first step in determining COGS for a manufacturing company is to establish the cost of materials placed into production. This is the amount of materials the company takes from materials inventory and puts into production. The formula to calculate this is shown in Formula 1.1.

|

Guided Example

For your example, determining cost of materials placed into production would look like this:| Beginning Materials Inventory | $ 450,000 | |

| + | Purchases | + $ 750,000 |

| - | Ending Materials Inventory | - $ 420,000 |

| Cost of Goods Placed into Production | $ 780,000 | |

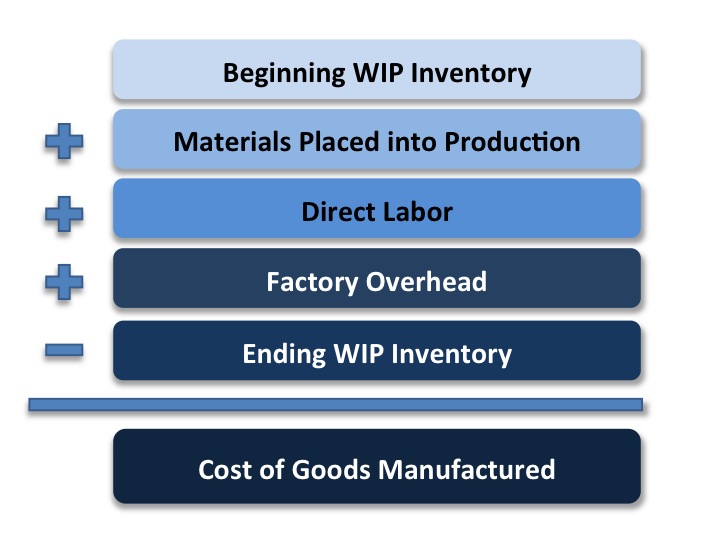

Step 2: Cost of Goods Manufactured

The next step in calculating COGS is to determine the cost of goods manufactured (COGM). This is the goods that have been completed. You find this by using the work in process inventory (WIP). WIP inventory is the amount of product that has been started but not yet completed. To WIP inventory, add the entire product costs, which included direct materials (which you found from the previous formula), direct labor and factory overhead. The formula for COGM is shown in Formula 1.2.

|

Guided Example

For your example, the COGM is shown below.| Beginning WIP Inventory | $ 200,000 | |

| + | Materials Placed into Production | + $ 780,000 |

| + | Direct Labor | + $ 300,000 |

| + | Factory Overhead | + $ 150,000 |

| - | Ending WIP Inventory | - $ 300,000 |

| Cost of Goods Manufactured | $ 1,130,000 | |

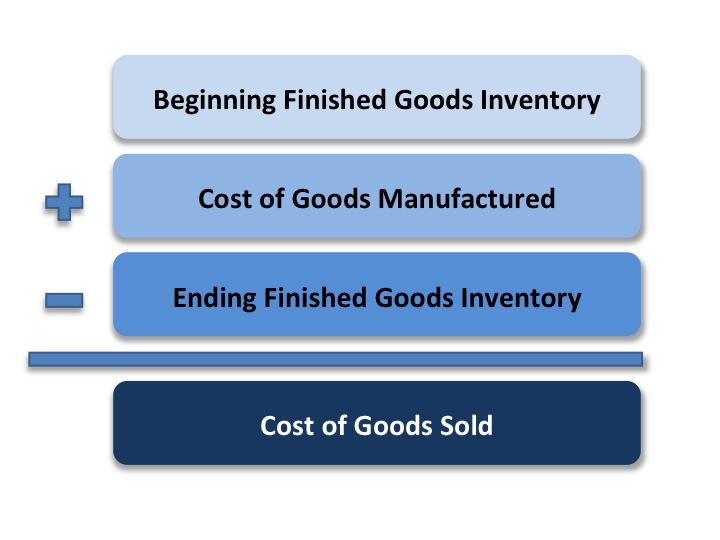

Step 3: Cost of Goods Sold

The final step is to calculate the cost of goods sold (COGS). This step includes the finished goods inventory, which is the inventory that accounts for goods that have been manufactured but not yet sold. You will add to it the goods that you completed this period (COGM, which is found in Formula 1.2). The formula is shown below.

|

Guided Example

For your example, the COGS is shown below.| Beginning Finished Goods Inventory | $ 400,000 | |

| + | Cost of Goods Manufactured | +$ 1,130,000 |

| - | Ending Finished Goods Inventory | - $ 350,000 |

| Cost of Goods Sold | $ 1,180,000 | |

Calculating COGS

Self-Check Activity

Use the following business information to practice calculating the cost of goods sold. Enter the necessary numbers in the boxes below, then click the "Show Answer" button after each step to ensure that your calculations are correct.

Self-Check Business Information

| Beginning Direct Materials Inventory | $ 650,000 |

| Ending Direct Materials Inventory | $ 480,000 |

| Direct Materials Purchases | $ 870,000 |

| Beginning Work in Process Inventory | $ 150,000 |

| Ending Work in Process Inventory | $ 250,000 |

| Direct Labor | $ 400,000 |

| Factory Overhead | $ 200,000 |

| Beginning Finished Goods Inventory | $ 500,000 |

| Ending Finished Goods Inventory | $ 450,000 |

HINT: Hover your mouse pointer over a step number below to view the step's formula if you need it.

STEP 1: Determine the Cost of Materials Placed into Production

|

|

|

STEP 2: Determine the Cost of Goods Manufactured

|

|

|

|

|