Main Content

Lesson 1: Introduction to Taxation and How to Research

The Internal Revenue Service

The Internal Revenue Service (IRS) is the agency of the Department of the Treasury of the U.S. government that takes responsibility for administering the U.S. tax law. It was created during the Civil War to help collect the income tax imposed to fund the war. However, it rose to its current prominence with the ratification of the 16th Amendment. The IRS is charged to do two things:

- Create the Internal Revenue Code.

- Police the tax law.

Create the Internal Revenue Code

The IRS creates and maintains the codification of tax law. When Congress creates a law, it isn’t organized and outlined for research purposes and easy reading. One of the roles of the IRS is organizing the law so that like subject matters are grouped together and properly coded for ease of research and citation.

You'll see the Internal Revenue Code (IRC) very soon when we look at tax research. Here is more information on the tax code itself.

In 1954, the tax law was codified to organize its specific laws for easier reference. Up to that point, laws were simply written. In order to find a statement pertaining to a certain tax issue, an attorney might have to read the entire document because there was no system in place to categorize the laws. (Some laws are thousands of pages long!) With minor changes made each year, the 1954 Code remained relatively stable until 1986.

In 1986, the Tax Reform Act of 1986 (TRA86) brought major changes to the IRC, which significantly changed the way individuals were taxed and set forth precedents that remain in effect today.

In 2001, the Bush Tax Act set forth incremental changes in the law that focused on tax savings for people who created jobs or positively impacted the U.S. economy. Because most of those people were wealthy, this act has been described as favoring the rich while penalizing the middle class.

In December 2017, the most sweeping tax reform since TRA86 became law. The new law signed by President Trump, the Tax Cuts and Jobs Act, significantly changed the tax law for both businesses and individuals. You will be learning this new law and its application throughout this coming semester.

As you can see, tax law changes continuously, and it is mandatory that tax professionals keep current on a daily basis—and sometimes even that isn't enough.

Police the Tax Law

The IRS, for the most part, helps law-abiding citizens report their information correctly so that they act in accordance with the law. However, the IRS is also charged with making sure citizens who are not following the law are identified and penalized.

In this course, we're focusing on individual (not business) taxes, so consider the federal income tax form that you complete each spring. The IRS created that form and others to make sure individuals report their tax information according to the law. After you submit your form, the IRS is responsible for making sure you, in fact, followed the law. As a part of this process, the IRS conducts audits when clarification is necessary or when it appears a taxpayer has not followed the tax law.

Audits are a part of the required enforcement responsibility of the IRS and are something most taxpayers fear. However, most IRS audits are not scary at all. Here are the different types of audits the IRS conducts.

Correspondence Audit

This is the most common type of audit. It occurs when the IRS finds a small discrepancy on a taxpayer’s tax return. The IRS notifies the taxpayer by letter to request information to resolve the issue. The taxpayer then responds by mail either to provide the information or to make further clarification. It's through this correspondence that the IRS and taxpayer resolve the issue, with the taxpayer possibly receiving a refund, paying additional tax, or having no change made to the tax amount.

Office Audit

This is an audit conducted at the taxpayer's IRS regional office. This type of audit is usually conducted when more information is needed than the IRS can resolve by mail. A face-to-face meeting is then conducted at the IRS regional office to resolve the issues.

Field Audit

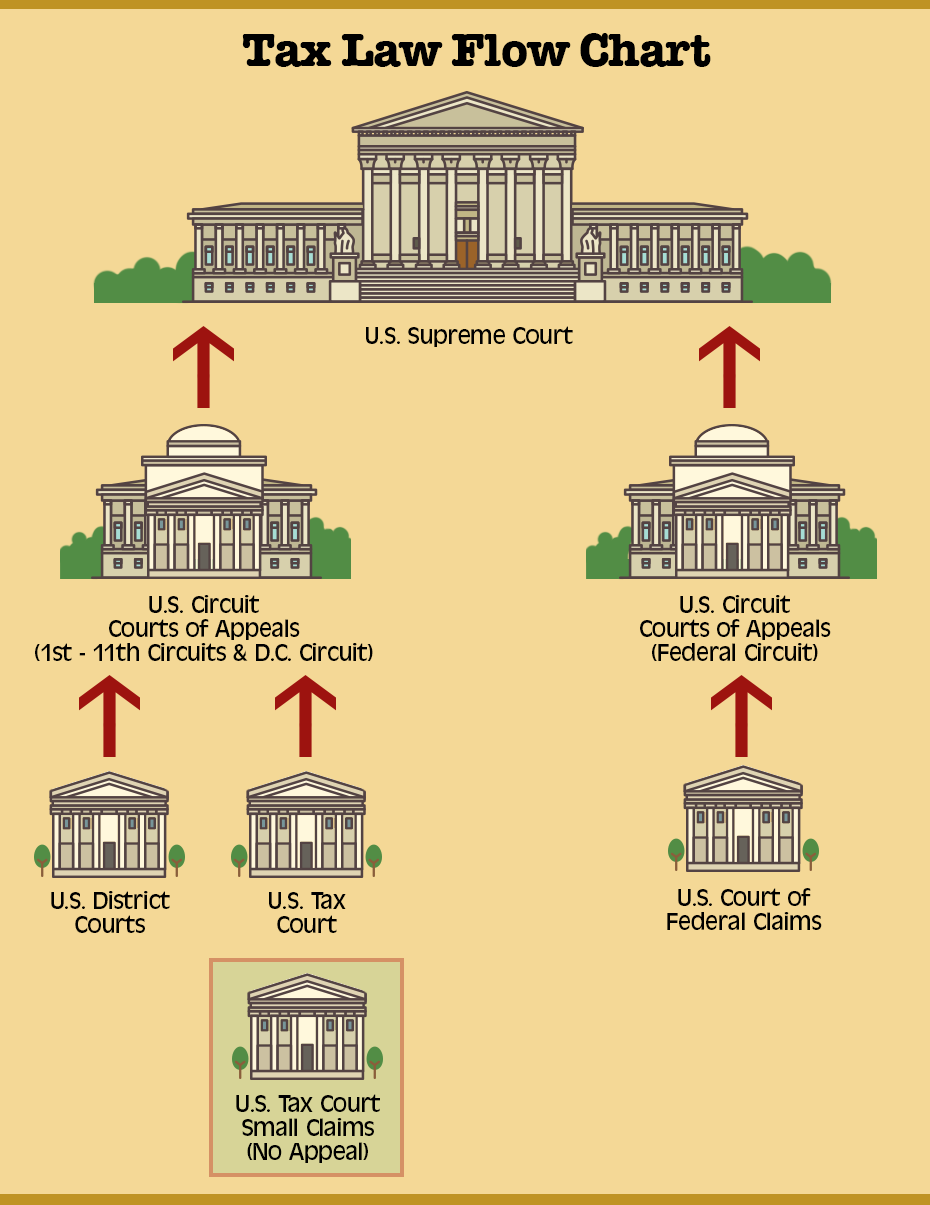

This happens when the IRS needs to look at significant items on the tax return and requires the audit to be conducted at the taxpayer’s residence or place of business. When an office or field audit is completed, the internal revenue agent prepares a report of the audit's findings. If the taxpayer doesn't agree with these findings, then they have a legal remedy by disputing them in tax court. There are different tax courts where a taxpayer can file a lawsuit, as well as different levels of appellate courts. Some cases may even make it to the Supreme Court.

Income Tax Disputes in Court

Figure 1.2 shows the courts used for federal income tax disputes. Note that there is a court of small claims where taxpayers who have small issues to resolve can plead their cases. Decisions that have been made through the small claims court may not be appealed to a higher court, however.

Remember that the IRS is like the police of the tax law, which means it isn't the final word. The federal tax system works the same way traffic law does: Whether you disagree with a speeding citation or an IRS audit, you can go to court to have it resolved.

So, now that you know how tax law is created by the federal government and administered by the IRS, what other types of taxes are there?