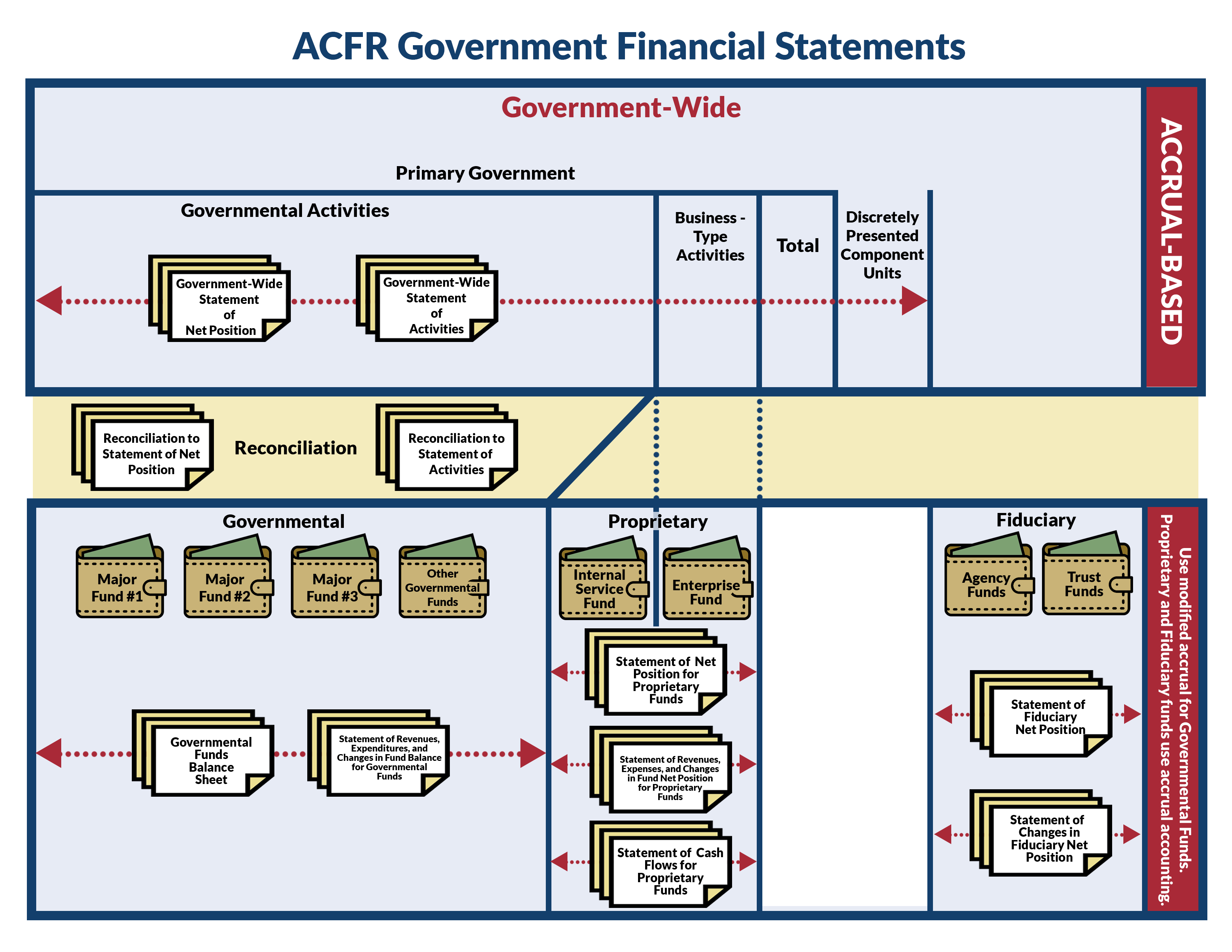

Main Content

Lesson 03: Modified Accrual Accounting: Including the Role of Fund Balances and Budgetary Authority

Modified Accrual Accounts

The Account Structure of Governmental Funds statement below (Illustration 3-1 in your textbook) displays the basic account structure for modified accrual accounting. The top section illustrates balance-sheet accounts. With several notable exceptions, the balance-sheet accounts are similar to those used in accrual-based accounting.

| Panel 1. Accounts that are not closed at year-end (Balance Sheet) | |

| Assets | Liabilities |

| Cash and Cash Equivalents | Accounts Payable |

| Investments | Accrued Liabilities |

| Receivables: | |

| Taxes Receivable | Deferred Outflow of Resources |

| Accounts Receivable | Deferred Tax Revenues |

| Due from Other Governments | |

| Supplies Inventories | Fund Balances |

| Restricted Assets (typically cash) | Non-spendable |

| Restricted | |

| Deferred Inflow of Resources | Committed |

| Assigned | |

| Unassigned | |

| Panel 2. Accounts that are closed at year-end | |

| Budgetary Accounts | Activity Accounts |

| Estimated Revenues | Revenues |

| Tax Revenues | |

| Charges for Services | |

| Appropriations | Expenditures |

| Current | |

| Capital Outlay | |

| Debt Service | |

| Estimated Other Financing Sources | Other Financing Sources |

| Transfers In | |

| Debt Proceeds | |

| Estimated Other Financing Uses | Other Financing Uses |

| Transfers Out | |

| Encumbrances | |

There are no equity accounts. Rather, since there is no ownership interest in the resources and obligations of the government, modified accrual accounting utilizes fund balance, defining it as the difference between assets and liabilities. Fund balance can then be broken down into five categories, which will be discussed later.

There are also no long-term-asset or long-term-liability accounts. Assets represent cash and other resources that will be converted to cash in the normal course of operations. Liabilities represent those obligations that will be settled with current financial resources. Deferred inflows and outflows are also additional accounts that are maintained on the governmental balance sheet. They are not the same as an asset or liability. The It Figures Podcast: S4:E14—Demystifying Deferrals from the CRI website talks about how difficult it can be to get them correct in the real world.

The lower section of the Account Structure of Governmental Funds statement displays activity accounts and budgetary accounts. Activity accounts represent the sources and uses of funds. Revenues and other financing sources are inflows of financial resources. Because taxes and other revenues don't involve exchange transactions, the concept of "earning" revenues is irrelevant. Revenues are recognized when the resources are considered measurable and available to finance expenditures of the current period. Other financing sources include transfers in from other funds and proceeds from long-term borrowing.

Expenditures and other financing uses (scroll up to view) are outflows of financial resources. The GASB defines expenditures as decreases in net financial resources. The recognition of expenditures in governmental funds occurs in accordance with the modified accrual basis of accounting. Therefore, expenditures in governmental funds are recognized when a liability is incurred that will be settled with current financial resources. Examples include salaries, equipment purchases, and payment of interest and principle on debt. There are no expenses. Other financing uses represent transfers to another fund. A transfer is a legally authorized movement of monies between funds. Transfers to other funds result in the reduction of one fund's expendable resources and an increase in another fund's resources; however, they are not expenditures.

The GASB requires that general- and special-revenue funds with legally adopted budgets provide reports comparing actual results with budgeted results. However, the GASB does not mandate specific procedures for doing so. Most governments typically record budgets in their formal journal entries. Commonly used budgetary accounts are displayed in Panel 2 of the Account Structure of Governmental Funds statement (scroll up to view). Estimated revenues represent those revenues anticipated to be raised in accordance with the legally adopted budget. Appropriations represent the legal authorization for the government to spend funds in accordance with the budget. Contrary to a business, the amounts spent cannot legally exceed the amounts appropriated for each approved purpose. Estimated other financing sources and estimated other financing uses represent anticipated inflows and outflows of resources other than revenues and spending. Examples include transfers into and out of other funds and proceeds received from the issuance of debt. An encumbrance (scroll up to view) represents a commitment to expend resources in accordance with a purchase order or contract. An encumbrance becomes a liability when the ordered product or service has been received.