ACCTG462:

Lesson 03: Modified Accrual Accounting: Including the Role of Fund Balances and Budgetary Authority

Lesson 3 Overview

This lesson will describe the basic accounts used by state and local governments and how to start using those accounts in the preparation of journal entries. Additionally, it will review how and when revenues and expenditures are recognized in governmental funds. Finally, it will define the different subsections or categories of fund balance.

Objectives

After completing this lesson, you should be able to

- identify when and how revenues and expenditures are recognized using modified accrual accounting,

- classify the segments of the fund balance for a governmental fund, and

- prepare journal entries using modified accrual accounting.

Important concepts include

- the difference between exchange and non-exchange transactions,

- revenue recognition,

- encumbrances,

- categories/restrictions of fund balance,

- sources and uses of funds, and

- budgets.

Lesson 3 Readings and Activities

By the end of this lesson, make sure you have completed the readings and activities found in the Lesson 3 Course Schedule.

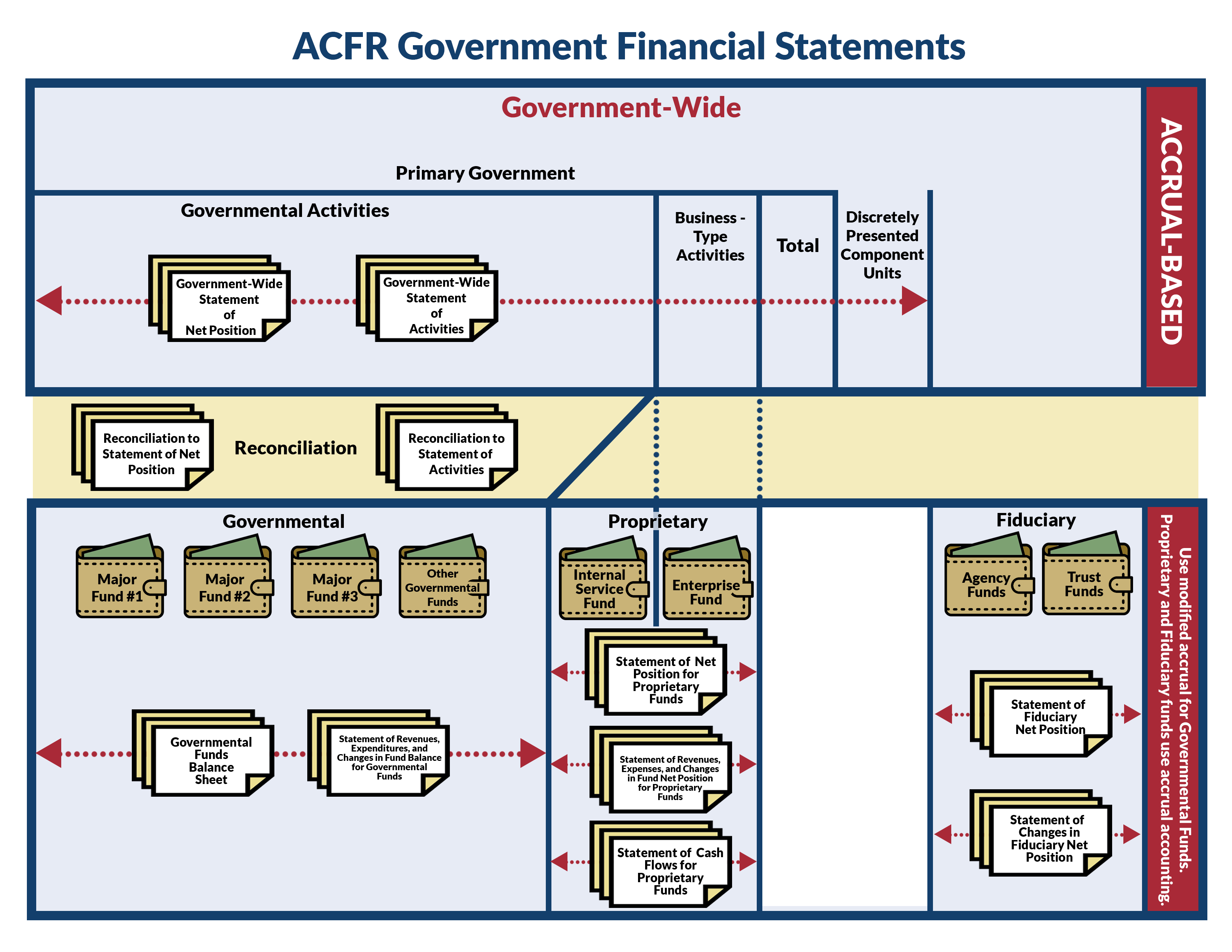

Modified Accrual Accounts

The Account Structure of Governmental Funds statement below (Illustration 3-1 in your textbook) displays the basic account structure for modified accrual accounting. The top section illustrates balance-sheet accounts. With several notable exceptions, the balance-sheet accounts are similar to those used in accrual-based accounting.

| Panel 1. Accounts that are not closed at year-end (Balance Sheet) | |

| Assets | Liabilities |

| Cash and Cash Equivalents | Accounts Payable |

| Investments | Accrued Liabilities |

| Receivables: | |

| Taxes Receivable | Deferred Outflow of Resources |

| Accounts Receivable | Deferred Tax Revenues |

| Due from Other Governments | |

| Supplies Inventories | Fund Balances |

| Restricted Assets (typically cash) | Non-spendable |

| Restricted | |

| Deferred Inflow of Resources | Committed |

| Assigned | |

| Unassigned | |

| Panel 2. Accounts that are closed at year-end | |

| Budgetary Accounts | Activity Accounts |

| Estimated Revenues | Revenues |

| Tax Revenues | |

| Charges for Services | |

| Appropriations | Expenditures |

| Current | |

| Capital Outlay | |

| Debt Service | |

| Estimated Other Financing Sources | Other Financing Sources |

| Transfers In | |

| Debt Proceeds | |

| Estimated Other Financing Uses | Other Financing Uses |

| Transfers Out | |

| Encumbrances | |

There are no equity accounts. Rather, since there is no ownership interest in the resources and obligations of the government, modified accrual accounting utilizes fund balance, defining it as the difference between assets and liabilities. Fund balance can then be broken down into five categories, which will be discussed later.

There are also no long-term-asset or long-term-liability accounts. Assets represent cash and other resources that will be converted to cash in the normal course of operations. Liabilities represent those obligations that will be settled with current financial resources. Deferred inflows and outflows are also additional accounts that are maintained on the governmental balance sheet. They are not the same as an asset or liability. The It Figures Podcast: S4:E14—Demystifying Deferrals from the CRI website talks about how difficult it can be to get them correct in the real world.

The lower section of the Account Structure of Governmental Funds statement displays activity accounts and budgetary accounts. Activity accounts represent the sources and uses of funds. Revenues and other financing sources are inflows of financial resources. Because taxes and other revenues don't involve exchange transactions, the concept of "earning" revenues is irrelevant. Revenues are recognized when the resources are considered measurable and available to finance expenditures of the current period. Other financing sources include transfers in from other funds and proceeds from long-term borrowing.

Expenditures and other financing uses (scroll up to view) are outflows of financial resources. The GASB defines expenditures as decreases in net financial resources. The recognition of expenditures in governmental funds occurs in accordance with the modified accrual basis of accounting. Therefore, expenditures in governmental funds are recognized when a liability is incurred that will be settled with current financial resources. Examples include salaries, equipment purchases, and payment of interest and principle on debt. There are no expenses. Other financing uses represent transfers to another fund. A transfer is a legally authorized movement of monies between funds. Transfers to other funds result in the reduction of one fund's expendable resources and an increase in another fund's resources; however, they are not expenditures.

The GASB requires that general- and special-revenue funds with legally adopted budgets provide reports comparing actual results with budgeted results. However, the GASB does not mandate specific procedures for doing so. Most governments typically record budgets in their formal journal entries. Commonly used budgetary accounts are displayed in Panel 2 of the Account Structure of Governmental Funds statement (scroll up to view). Estimated revenues represent those revenues anticipated to be raised in accordance with the legally adopted budget. Appropriations represent the legal authorization for the government to spend funds in accordance with the budget. Contrary to a business, the amounts spent cannot legally exceed the amounts appropriated for each approved purpose. Estimated other financing sources and estimated other financing uses represent anticipated inflows and outflows of resources other than revenues and spending. Examples include transfers into and out of other funds and proceeds received from the issuance of debt. An encumbrance (scroll up to view) represents a commitment to expend resources in accordance with a purchase order or contract. An encumbrance becomes a liability when the ordered product or service has been received.

Classifications of Fund Balance

A fund balance for governmental funds is analogous to equity for a business and possesses the following characteristics:

- activity accounts are closed to this account at the end of each accounting period,

- the balance represents the net resources that are available for future spending, and

- the categories within the fund balance represent the different constraints to which government managers must adhere.

There are five categories of fund balance:

- Non-spendable resources are resources that cannot be spent, including

- inventories,

- prepaid expenses, and

- the principal of a permanent fund.

- Restricted funds are funds that have constraints placed upon them by external parties regarding the use of resources. These constraints can be

- externally imposed (through a debt covenant, a grantor, contributors, or other governments), or

- imposed by law (constitutionally or through enabling legislation).

- Committed funds are those with constraints placed on the use of resources by

- formal action of the government’s highest level of decision-making authority or

- contractual obligations.

- Assigned funds are those for which the government has an expressed intent to use resources for specific purpose.

- No formal action has been taken by the government's highest level of decision-making authority. For example, if a controller decides staff members need Excel training and expresses an intent to spend $30,000 next year on the training, but the legislature has not taken action on this intent, the $30,000 would be part of assigned funds.

- For government funds other than the general fund, this is the last category for all remaining positive amounts.

- Unassigned funds are those that have no constraints placed on them and that are a residual classification of the general fund.

- Only the general fund can report a positive unassigned fund balance.

- For government funds other than the general fund, this is used only to report a negative balance.

Test Yourself

Rainy-day funds are sometimes referred to as budget-stabilization funds.

Question: The government sets aside $100,000 as a rainy-day fund for plowing and salting the roads in case the winter is worse than expected. When would this be considered a committed fund?

Expenditure-Cycle Journal Entries

Expenditure-cycle journal entries are presented in Illustration 3-4 in your textbook.

Budget Approval

As shown in Illustration 3-4, the first step is the recording of the legally adopted budget. Estimated revenues and estimated other financing sources are represented as debits. Appropriations and other financing uses are represented as credits. Budgetary fund balance can be debited or credited and is determined by the excess (or deficiency) of debits over credits in the other accounts. A credit to the budgetary-fund-balance account represents an anticipated increase in the fund balance of the fund, while a debit to the account represents an anticipated decrease in the fund balance of the fund.

Purchase Order Issued

When an item or service is ordered, an encumbrance is journalized to indicate that a commitment to expend resources has been made. An encumbrance is debited, while the budgetary fund balance (reserve) for encumbrances is credited.

Example

The city of Sunbury, Pennsylvania, placed a purchase order for a new police car. The expected cost of the car is $75,000. Prepare the appropriate entry to record the purchase order for the new police car.

Goods and Services Received

Once the item or service has been received, the corresponding encumbrance is reversed, with the appropriate expenditure and liability recorded.

Example

The new police car was delivered to the city. The final invoice price of the car was $76,250. Prepare the appropriate entries to record the expenditure.

Revenue Recognition

Modified accrual accounting dictates that revenues for non-exchange transactions be recognized when they are measurable and available to fund operations of the current period. Non-exchange transactions are those in which the government receives resources without giving something of equal value in exchange for those resources. The most common example would be tax revenues.

Before a government can recognize non-exchange revenues, any eligibility requirements must first be met. Those requirements fall into the following categories:

- Required characteristics of recipients: If the provider of the resources specifies the characteristics of those to benefit from the resources, those requirements must be met. For example, a grant may specify that beneficiaries be minority-owned businesses.

- Time requirement: If the provider of the resources specifies when resources must be spent, those requirements must be met. For example, a donor may specify that funds be spent on cemetery maintenance during the next year. The gift would be recognized as revenue that next year.

- Reimbursement: Many grants and gifts promise to reimburse governments for qualified expenditures. The revenue will not be recognized until the expenditures have been made.

- Contingencies: Resources that have a contingency attached do not get recognized as revenue until the contingency has been met. For example, a donor may pledge a gift of $1,000,000 to support construction of a new park if the city can raise an additional $1,000,000 from other sources. Until the city raises the additional funds, it cannot recognize the donor's gift as revenue.

Non-exchange transactions fall into four categories: imposed non-exchange transactions, derived tax revenues, government-mandated non-exchange transactions, and voluntary non-exchange transactions (described below). Specific journal entries for each type of non-exchange transaction are presented in Illustration 3-5 in your textbook.

- Imposed non-exchange transactions involve taxes and other assessments that don't result from an underlying transaction. Examples include property taxes and fines. Property taxes are considered available to finance current-year expenditures if they are collected within 60 days after the end of the current fiscal year. As such, they will be considered revenue for the current year. Any property taxes expected to be collected after 60 days following the end of the fiscal year will be deferred until the next year.

- Derived tax revenues involve taxes based on exchange transactions conducted by businesses and citizens. Examples include sales taxes (based on sales of goods and services), income taxes (based on income earned by citizens and businesses), and excise taxes (based on sales of specific goods such as gasoline).

- Government-mandated non-exchange transactions are grants from higher levels of government that support required programs.

- Voluntary non-exchange transactions are donations and grants that support a voluntary program.

| Type | Description and Examples | Modified Accrual Basis (Governmental Fund Basis) | Representative Transactions | Sample Journal Entry (Governmental Fund-Basis Reporting) |

| Imposed Non-exchange Revenues | Taxes and other assessments that do not result from an underlying transaction. Examples include property taxes and special assessments imposed on property owners. Also includes fines and forfeits. |

Record the receivable (and an allowance for uncollectibles) when an enforceable claim exists. Revenues should be recognized in the period for which the taxes are levied (i.e., budgeted), but are also subject to the availability rule. Property tax revenues expected to be collected over 60 days after year-end are deferred. |

1. Property taxes levied 2. Deferral of portion expected to be collected over 60 days after the year-end |

1. Taxes Receivable ............ Dr

2. Revenues Control ........... Dr

|

| Derived Tax Revenues | These are taxes assessed on exchange transactions conducted by businesses or citizens. Examples include sales, income, and excise taxes. |

Record the receivable when the taxpayer's underlying transaction takes place. Revenues should be recognized when available and measurable. Revenues not expected to be collected in time to settle current liabilities are deferred (i.e., available and measurable criteria). |

1. Income tax withholdings are received. 2. Additional income taxes expected to be received after year-end. Part of this will not be received in time to be available to settle current liabilities. |

1. Cash ......................................... Dr

2. Taxes Receivable ....................... Dr

|

|

Government-Mandated Non-exchange Transactions

Voluntary Non-exchange Transactions | Grants from higher levels of government (federal or state) given to support a program. Since the program is required, the lower-level government has no choice but to participate. Donations and grants given to support a program. Since the program is not required, the receiving government voluntarily agrees to participate. |

The recognition rules are the same for mandated and voluntary non-exchange grants. Record the revenue when all eligibility requirements have been met. In the case of reimbursement grants, revenue is recognized only when qualified expenditures have been incurred. In the case of advance funded grants, recognize revenues as qualified expenditures are incurred. | Reimbursement grant:

1. Incur qualified expenditures. 2. Recognize revenue. —————————Advance funded grant: 3. Receipt of advance funding. 4. Incur expenditures and recognize revenue in an equal amount. |

1. Expenditures Control ................. Dr

2. Due from grantor ....................... Dr

3. Cash .......................................... Dr

4 a. Expenditures Control ............... Dr

4 b. Deferred Revenues—Grants ..... Dr

|

In this lesson, you have learned the criteria for recognizing revenues and expenditures for governmental funds, as well as some specific journal entries that a fund may record. In addition, the lesson defined the different categories of fund balance. Using what you've learned, proceed to the assignments in the next section.