Main Content

Lesson 1: Course Orientation and Review of Accounting Cycle

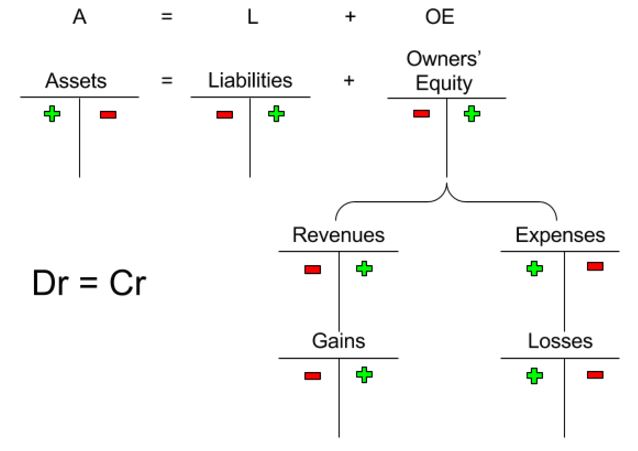

Double-Entry Accounting System

The double-entry system is a universally used system in accounting to ensure that debits equal credits. For every transaction that occurs, a company must record the two-sided effect of each, identifying the appropriate general ledger accounts affected. The double-entry system also serves a check-and-balance to ensure the accuracy of the records transaction amounts. If a company records every transaction with the equal number of debits and credits as it should, then the sum of the debit entries to all of accounts must, by rule, equal the sum of all of the credit entries.

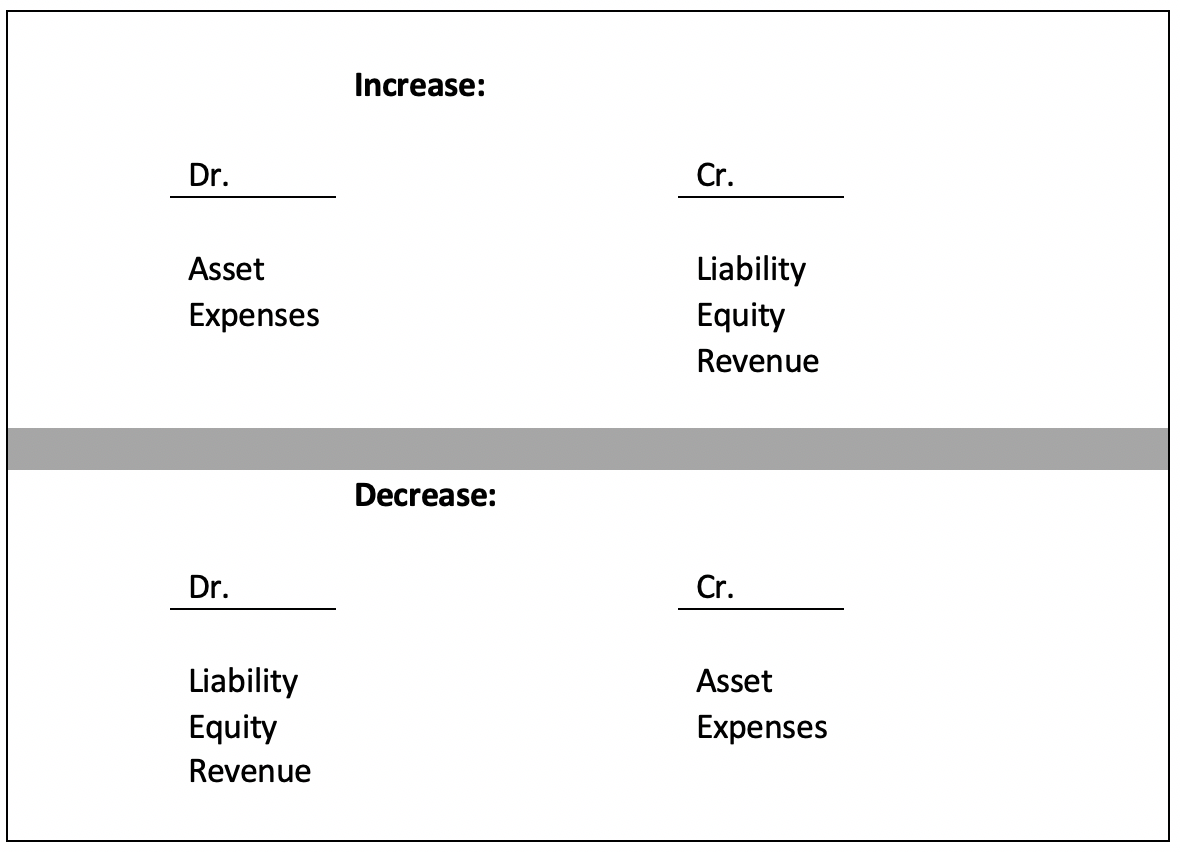

As shown on the illustrative example, there are certain specific rules that must be followed that are the foundation for the double-entry system.

- Increases in all asset and expense accounts are recorded on the left (or debit) side, and decreases in those same accounts on the right (or credit) side.

- On the other hand, increases in all liability and revenue accounts are recorded on the right (or credit) side, and decreases on the left (or debit) side.

Transactions affecting stockholders' equity will also be recorded in a similar manner.

- Increases to equity accounts, such as Common Stock and Retained earnings, are recorded on the credit side, while increases to Dividends are recorded on the debit side.

Double-Entry (Debit and Credit) Accounting System Self-Check Activity

Consider what the double entry should look like in a t-account. Then click on the Show Entry link to check your answers.

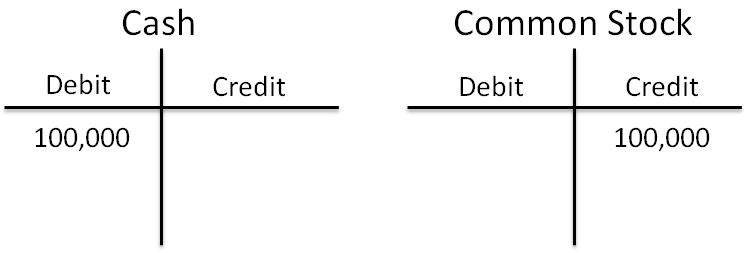

1. Owners invest $100,000 in the corporate form of a business. (Show Entry)

An investment of cash in a business represents an increase (or debit) to the company's cash balance. In return, the owners receive stock (or ownership) in the business for their investment.

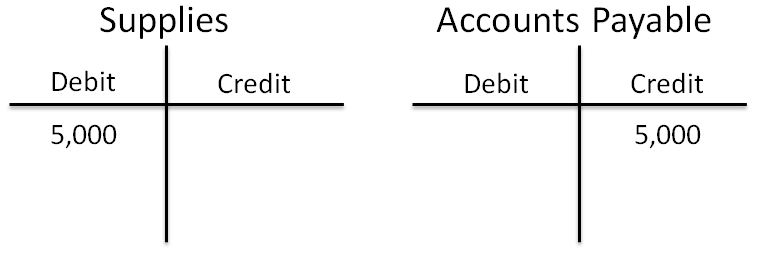

2. Company purchased $5,000 of supplies on account (Show Entry)

The purchase of supplies represents an asset to the company and does not become an expense until the supplies are used or consumed in the business. The asset account Supplies is increased, and since the supplies have not been paid for as yet, a credit (or increase) to the liability account is shown.

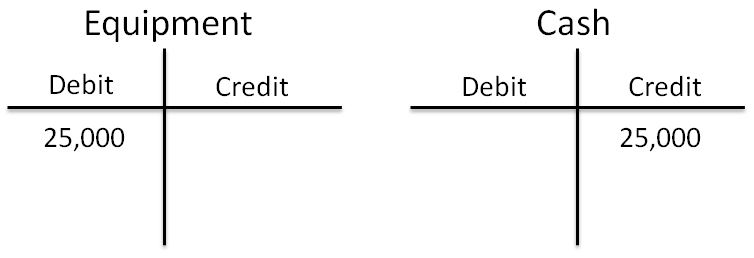

3. Purchased equipment in the amount of $25,000 for cash (Show Entry)

Equipment represents a long-term asset of the company. So when equipment is acquired, the asset account increases. Since the equipment was purchased for cash, the asset account Cash is decreased. This is an example of a transaction that only affects one side of the accounting equation (the asset side). However, equality of the transaction must still exist.

4. Rendered services for $15,000 cash (Show Entry)

Since the company has received cash, the asset account Cash is increased and the revenue account, which indirectly flows through stockholders' equity, is credited.

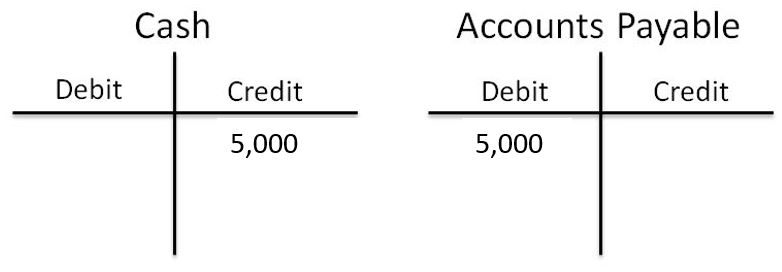

5. Paid vendor for supplies purchased in Problem 2 (above) (Show Entry)

Since the company has paid the vendor with cash for supplies that were previously purchased on account, the asset account Cash is decreased. In addition, the liability account Accounts Payable is also decreased (or debited) since the supplies that were purchased in Transaction 2 have been paid for in full. It should be noted that the balance in the Accounts Payable account is now zero.