FIN513:

Lesson 2 - Part 1

Overview

Marathon Petroleum Corporation (NYSE: MPC), a U.S. based oil refining, marketing, and pipeline transport company, has a refining capacity in excess of 1 million barrels of oil per day. MPC needs crude oil every day and it may purchase it in one of two ways:

- Wait until a future date when MPC needs crude oil, and then buy crude oil in the spot market at the market price, or

- Enter into a long-term contract today for delivery of crude oil (forward contract) on a specified future date.

On 1/9/2012, the crude oil spot price is $98/bbl and the interest rate 6%.

Suppose MPC entered into a long-term contract (forward contract) on January 9, 2012 with Exxon to buy 1,000,000 barrels for delivery on September 1, 2012. The delivery price agreed for the contract is $100 a barrel. This means MPC will obtain 1,000,000 bbls on September 1, 2012 at a total cost of $100 million as agreed. What if the spot market price on 9/1/2012 is only $60 a barrel? Then MPC would have overpaid $40 million for the 9/1/2012 delivery compared to the spot price. What if the spot price is $120 a barrel instead? Then MPC would have paid $20 million less. (Of course, the supplier faces exactly the opposite situation.)

In other words, if MPC buys crude oil on the spot market, the cost of crude oil is uncertain, but the forward contract secures predictability of the cost of crude oil for MPC.

MPC, the buyer of the forward contract, is called to have a "long" position, and the supplier, the seller, a "short" position.

The main questions to think about in this lesson are:

- How would you check if the forward price of $100 is arbitrage-free? [Hint: Devise an equivalent forward contract on 1/9/2012 using the crude oil spot market and the financial market for borrowing or lending. To simplify the analysis, assume the storage cost of crude oil is zero.]

- How do you determine the value of MPC's long position for the September 1st delivery on any date before September 1st, 2012?

- on Jan 9, 2012? [Hint: value > 0. Why and how much?]

- on September 1, 2012 when the spot price is $120? [Hint: $20m. Why?]

- on March 1, 2012 when the spot price is $90? [Hint: value < 0. Why and how much?]

Learning objectives:

After completing this lesson, you will be able to:

- understand the concept and payoff profiles of a forward contract;

- price a forward contract on an asset with and without known amount of income;

- price a forward contract on an asset with known yield, not the amount;

- value an existing forward position on an asset with and without known amount of income; and

- value an existing forward position on an asset with known yield, not the amount.

Forward Contract (Concept)

Forward Contract: An agreement to BUY or SELL an asset at a specified time (maturity or settlement date) in the future for a specified price.

The buyer of a forward contract agrees to pay a specified amount at a specified date in the future in exchange for a specified asset (called the "underlying"), such as currency, commodity, interest payment, bond, etc.

Example 2.1. (MPC):

On Jan 9, 2012, MPC agreed to take a delivery of 1 million barrels of crude oil on Sept. 1, 2012 at $100 a barrel from Exxon, regardless of the prevailing spot price on 9/1/2012.

- MPC is the buyer – the counter party taking a LONG position

- Exxon is the seller – the counter party taking a SHORT position

- The specified asset (commodity) is the crude oil, the specified time of the delivery date is 9/1/2012, and the specified price is $100 per barrel

- MPC will pay $100/bbl on 9/1/2012 regardless of the prevailing spot price

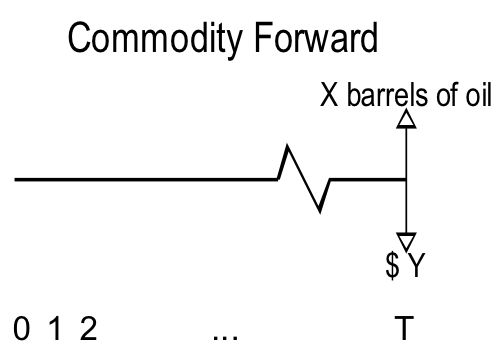

The exchange of the "underlying" and the "price" at the settlement time, T, can be viewed in the following figures:

Note: Click on the dots below to navigate through the content within the slide sorter.

Commodity forward contract: the underlying is a commodity such as a certain amount of crude oil, gold, corn, etc. in exchange for an agreed price.

Figure 2.1. Commodity Forward Contract

FX forward contract: the underlying is the a fixed amount of foreign currency, such as 1 million yen, in exchange for an agreed price in USD.

Figure 2.2. Foreign Exchange Forward Contract

Interest forward contract: Receive the interest based on the spot LIBOR rate (floating rate is the underlying) at maturity on a notional principal of, let's say $10 million, and receive an agreed fixed rate of 5%.

Figure 2.3. Interest Rate Forward Contract

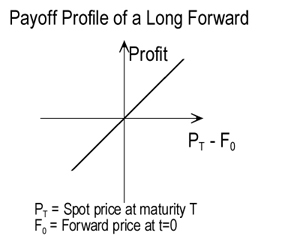

Payoff Profile of a Forward Contract

Example 2.2.:

The forward price of the MPC forward contract (Example 2.1.) was F0 = $100 /bbl.

- MPC will gain if the spot price of the crude oil on T= 9/1/2012 is PT > $100. The gain will be (PT - F0) per bbl.

- MPC will lose if the spot price of the crude oil on T= 9/1/2012 is PT < $100. The loss will be (F0 - PT) per bbl.

- MPC's payoff profile is along the 45 degree line in Figure 2.4 (Long Forward Payoff - see below).

- The payoff profile for Exxon, the seller, is along the negatively sloped 45 degree line in Figure 2.5 (Short Forward Payoff - see below) - exactly opposite to MPC's (zero sum game).

Figure 2.4.: Long Forward Payoff

Figure 2.5.: Short Forward Payoff

What Should be an Equilibrium Forward Price?

Example 2.3. (Creating a Synthetic Long Gold Forward):

The following steps create a situation with the delivery of gold and cash flow identical to a long gold forward contract – creates synthetically a gold forward long contract. The spot price of gold today, S0, is $1,000/oz. The risk-free interest rate, R0, is 6% and the gold lease rate, I0, is 2%/year, payable at the end of the lease period.

- Borrow money S0 = $1,000 for one year

- Buy gold in the spot market

- Lend the gold for one year

- At the end of one year, pay the loan, collect the gold and the fee from lending the gold, and you have the gold

This is equivalent to a long gold forward contract with zero cash flow at the beginning and a payment for the underlying at the settlement:

→ t = 0: CF0 = +$1,000 (loan) - $1,000 (pay for Gold) = 0

No gold in possession – b/c the gold bought was lent→ t = 1: Pay back the loan and collect the gold rental fee

CF1 = - 1,000 · (1 + 6%) + 1,000 · 2% = -$1,040

Get back the gold: + Gold(1oz)→ The net amount to pay is:

FSYNTHETIC = (spot price) + (interest cost) – (gold lease fee)

= S0 · (1 + R0 - I0) = 1,000 · (1 + 6% - 2%) = $1,040

What Should be an Equilibrium Forward Price? (continued)

- If two portfolios have identical cash flows (equivalent), the arbitrage-free condition requires that the two portfolios must be priced the same.

-

Forward Prices reflect Costs and Benefits:

(Forward Price)

= (Spot Price) + FV of {(cost - benefits) for deferred transaction}

Example 2.3. continued (Arbitrage-free and Forward Price, F0):

Arbitrage-free condition will require the gold forward price to be equal to the synthetic gold forward cost:

F0 = FSYNTHETIC (= $1,040)

What if a dealer quotes a gold forward price of F0 = $1,100 (higher than $1,040)?

Click on Example 2.3. Solution with gold forward price of F0= $1,100 (higher than $$1,040) to view the solution.

Example 2.3. Solution with gold forward price of F0 = $1,100 (higher than $1,040):

At t = 0: Short forward + Long synthetic forward

At t = 1 (one year later):

- Short forward at F0 = $1,100

- Borrow S0 = $1,000 at 6% +$1,000

- Buy gold spot at S0 = $1,000 -$1,000

- Lease the gold at 2%

→ Net CF0 = zero; no gold in possession

- Pay back the loan and accrued interest = - $1,000 · 1.06 = - 1,060

- Receive accrued fee on gold lease: 1,000 · 2% = $20

- Close the short forward position:

Deliver gold for F0 = $1,100 +$1,100- Net Profit +$60

This is a risk-free profit with no initial investment - pure arbitrage profit!

As long as F0 > FSYNTHETIC, this strategy will yield an arbitrage profit, driving F0 down to FSYNTHETIC

What if the dealer quotes a gold forward price of F0 = $1,020?

Click on Example 2.3. Solution with gold forward price of F0= $1,020 to view the solution.

Example 2.3. Solution with gold forward price of F0 = $1,020:

At t = 0: Long forward + short synthetic forward

- Long forward at F0 = $1,020

→ Net CF0 = zero; no gold in possession- Borrow gold at 2%

- Sell gold spot at $1,000 +$1,000

- Deposit $1,000 at 6% -$1,000

At t = 1 (one year later):

- Close the long forward position:

Accept delivery of gold for F0 = $1,020 ($1,020)- Return borrowed gold with accrued fee: ($20)

- Get back the deposit with interest, S0 · (1+6%) +$1,060

- Net Profit +$20

This is a risk-free profit with no initial investment - pure arbitrage profit!

As long as F0 < FSYNTHETIC, this strategy will yield an arbitrage profit, driving F0 upward to FSYNTHETIC

Wrap-up: The arbitrage-free condition establishes the forward price as F0 = (spot price) + (interest cost) - (gold lease fee), i.e.

= S0 (1 + (R0 - I0)*t) or = S0 (1 + R0 - I0)t (discrete compounding)

= S0 EXP{(R0 - I0) · t} (continuous compounding)

The Net Present Value of Forward Contract

The forward price is such that NPV of an at-market Forward contract = 0

- Because an at-market forward has no arbitrage profit making opportunity

- Because the exercise price of a contract = PV(the spot price at t = 0, net of income from the underlying, plus carrying cost of the underlying)

Example 2.4. (of NPV Calculation of a Forward Contract):

The IBM stock is currently traded at $180. A stock dealer offers a 6-month forward (or futures) on IBM at $185.32.

Assume the risk-free rate, r0, is 6% and there will be no dividend payment within six months. How would you calculate the NPV of a long forward contract?

Click on Example 2.4. Solution to view the solution.

Under the long forward, the buyer will pay $185.32 and receive one share of IBM stock in 6 months. Therefore,

(NPV of the forward) = -PV($185.32) + PV (1 share of IBM stock in 6 months).

- PV($185.32) = $185.32/(1 + 6%)∧0.5 = 180

- One share of IBM stock in 6 month is financially equivalent to one share of IBM stock now because there is no dividend payment, which is worth $180 today, i.e., the PV(IBM share at maturity) = $180.

Therefore NPV = - 180 + 180 = 0

NPV of Forward Contracts: The forward price is such that NPV of an equilibrium-priced forward contract = 0

- Because an equilibrium-priced forward has no arbitrage profit making opportunity

= (the spot price at t = 0)

- FV(net of income from the underlying)

+ FV(carrying cost of the underlying)

Why Enter into a Forward Contract When NPV = 0?

- To reduce price risk to one party

- To benefit from expectation of price movement different from market's

- To create synthetic assets

Default risk in Forwards

- Forwards – low transaction cost but high performance risk (= credit risk)

- Participating in the forward market requires an access to credit line with substantial amount. Therefore, forwards markets are for institutions with access to credit line as a regular part of their business, such as large corporations and governments.

Forward – Pricing and Valuation: Forward Contracts on Underlying with No Income, No Storage Cost

| Variables | Meanings |

|---|---|

| T: | delivery time |

| r: | risk-free interest rate for maturity T |

| S0: | Spot price today, t = 0 |

| F(0,T): | forward price today (t = 0) with expiration at t = T |

| Vt1 (0,T): | Value at t = t1of an existing LONG forward contract expiring at t = T established at t = 0 < t1 (is this less than t1) |

Forward Price:

Recall: FowardPrice = SpotPrice + {FV(cost) - FV(benefits)} for deferred transaction.

FV(cost) is the interest cost of borrowing (assuming no storage cost), FV(benefit) = zero (assuming no income from the underlying).

Therefore:

- Discrete compounding: F(0,T) = S0 (1+r)T [⇔ FV(Spot Price at t = 0)]

Because (S0 (1 + r)T - S0) is the interest cost, we obtain:

S0 + (S0 (1 + r)T - S0) = S0 (1 + r)T - Continuous compounding: F(0,T) = S0erT [⇔ FV(Spot Price at t = 0)]

Lesson 2 Exercise 1: Application to the MPC Pricing Question in Overview

How would you check if the forward price of $100 is arbitrage-free? [Hint: Devise an equivalent forward contract on 1/9/2012 using the crude oil spot market and the financial market for borrowing or lending. To simplify the analysis, assume the storage cost of crude oil is zero.]

This exercise provides you with an opportunity to review some concepts of forward contracts on an underlying asset with no income, no storage cost. Please attempt to solve the question on your own and then submit your work to the Lesson 2: Exercise 1 Drop Box to retrieve the solution to the question. The solution is a locked file and can only be accessed once you have submitted your work to the Lesson 2: Exercise 1 Drop Box.

Review your answers in comparison to the solution. If you have wrong answers to the question, you should revisit the forward contracts concepts presented. And, if you still have difficulties understanding the material and why you made mistakes, please contact me.

Forward Contracts on Underlying with No Income, No Storage Cost (continued)

Present Value of an existing forward contract

Example 2.5. (Value of an Existing Forward Contract):

Consider the MPC's forward contract mentioned in the Overview of this lesson – MPC is long on a crude oil forward contract with contract priced at F(1/9/2012,9/1/2012) = $100/bbl since 1/9/2012. What would be the value of the MPC's long forward position on March 1, 2012 if the spot price on March 1st is $105 and the risk-free rate is 4%?

Click on Example 2.5. Solution to view the solution.

The market value of MPC's long position as of 3/1/2012 can be realized by taking a short position on 3/1/2012 leaving the net underlying = zero at the delivery time.

The forward price on March 1st for 9/1/2012 delivery is the FV of S3/1/2012, $105. Since it is 0.5 year between 3/1/2012 and 9/1/2012, we get:

- F(3/1/2012,9/1/2012) = 105 · EXP(4% · 0.5) = 107.12

- By selling on 3/1/2012 the forward contract (delivery 9/1/2012) at 107.12, on Sept 1. 2012 MPC will receive 107.12 from closing the short position and pay 100 from closing the long position. There will be no net delivery of the underlying as the long and short positions cancel out each other. Thus the market value of the MPC's long position, V3/1/2012(1/9/2012,9/1/2012), is the PV of $7.12, the difference between the forward price on March 1 and the forward price of the existing contract:

- V3/1/2012(1/9/2012,9/1/2012) = PV[F(3/1/2012,9/1/2012) - F(3/1/2012,9/1/2012)]

= (107.12 - 100) · EXP(-4% · 0.5) = $6.98- The market value of the forward contract made on 1/9/2012 at $100 is worth $6.98 on 3/1/2012.

Note: If you need further assistance in solving this example, view the Value of an Existing Forward Contract video by clicking on the Instructional Videos link in the left menu.

By formalizing this, the market value at t = t1 of a long forward position created earlier can be found through one of two approaches:

Click on Approach 1 Solution to view the solution.

Approach 1 Solution: Take an offseting short forward

Approach 1: Short forward at t = t1 as in the example above

- Short forward at t = t1: F(t1,T) = St1er(T-t1)

- CFs at maturity (T)

- Close the existing long forward: pay F(0,T) & receive the underlying

- Close the short forward: deliver the underlying & receive F(t1,T)

- The PV of the net proceeds:

- Vt1(0,T) = PV{F(t1,T) - F(0,T)}

= {(St1er(T-t1)) - F(0,T)}e-r(T-t1)

= St1 - F(0,T)e-r(T-t1)

Vt1(0,T) = SpotPrice(t1) - PV (the price of the existing forward) for an underlying asset with no income and no storage cost

Click on Approach 2 Solution to view the solution.

Approach 2 Solution: Short sell the underlying

Approach 2: Short sell the underlying at t = t1

- Borrow the underlying

- Sell it at the spot price of St1

- CFs at maturity (T)

- Close the long forward: pay F(0,T) & receive the underlying

- Close the short selling: return the underlying

- The two CFs are at two different points in time:

- +St1 at t=t1

- -F(0,T) at t=T

- Thus the PV of the two CFs at t = t1 is:

Vt1(0,T) = St1 - PV{F(0,T)} = St1 - F(0,T)e-r(T-t1)

Vt1(0,T) = SpotPrice(t1) - PV (the price of the existing forward)

Vt1(0,T) = PV{F(t1,T) – F(0,T)}

= {(St1er(T-t1) ) – F(0,T)}e-r(T-t1)

= St1 – F(0,T)e-r(T-t1)

Lesson 2 Exercise 2: Application to the MPC Valuation Question in Overview

How do you determine the value of MPC’s long position for the September 1st delivery on any date before September 1st, 2012?

- on Jan 9, 2012? [Hint: value > 0. Why and how much?]

- on September 1, 2012 when the spot price is $120? [Hint: $20m. Why?]

- on March 1, 2012 when the spot price is $90? [Hint: value < 0. Why and how much?]

This exercise provides you with an opportunity to review some concepts of forward contracts on an underlying asset with no income, no storage cost. Please attempt to solve the question on your own and then submit your work to the Lesson 2: Exercise 2 Drop Box to retrieve the solution to the question. The solution is a locked file and can only be accessed once you have submitted your work to the Lesson 2: Exercise 2 Drop Box.

Review your answers in comparison to the solution. If you have wrong answers to the question, you should revisit the forward contracts concepts presented. And, if you still have difficulties understanding the material and why you made mistakes, please contact me.

Lesson 2 Exercise 3: Pricing & Valuation (Don Chance page 44, Practice Problem 1)

An investor owns an asset valued at € 125.72. The investor plans to sell it in nine months to raise money, but he is concerned about the price risk. He took a short forward position on this asset with the delivery in 9 months. The risk-free interest rate is 5.625%.

- What should be the amount the investor should be able to receive from such a forward contract in 9 months?

- If the forward dealer quotes € 140, how can the investor take advantage of this? Annualized rate of return? Why the transaction is attractive?

- Suppose you took the short position at the forward price computed in (A) above. Two months later, the spot price of the asset is € 118.875. What is the market value of your short position in the forward contract at this point?

- What is the value of the forward contract at expiration assuming the contract is entered into at the price computed in (A) above? The spot price of the asset is € 123.50 at expiration. Explain how the investor did on the overall position of both the asset and the forward contract in terms of the rate of return.

This exercise provides you with an opportunity to review some concepts of forward contracts on an underlying asset with no income, no storage cost. Please attempt to solve the question on your own and then check the answers in the textbook. Finally, please submit your work to the Lesson 2: Exercise 3 Drop Box to retrieve the Excel solution. The Excel solution is a locked file and can only be accessed once you have submitted your work to the Lesson 2: Exercise 3 Drop Box. Note: The cells which are highlighted yellow within the Excel worksheet are input data.

Review your answers in comparison to the solution. If you have wrong answers to the question, you should revisit the forward contracts concepts presented. And, if you still have difficulties understanding the material and why you made mistakes, please contact me.

Copyright 2002, CFA Institute. Reproduced and republished from Analysis of Derivatives for the CFA Program by Don M. Chance, with permission from CFA Institute. All rights reserved.