Main Content

Lesson 2: Forward Contracts I Part 2

Forward - Pricing and Valuation

Forward Contract on Investment Assets with Known Dollar Income

Note: If you need further assistance in understanding this concept, view the Forward Contract on Asset with One-time Known Income video by clicking on the Instructional Videos link in the left menu.

The Issue: If the underlying asset of a forward contract has income before the maturity of the forward contract, a synthetic forward method requires adjustments with the income. The table below compares cash flows between the forward (top half) and the synthetic forward (bottom half).

| Forward | t = 0 | t = 3 mo | t = 9 mo |

|---|---|---|---|

| -- | -- | -- | - F(0,9) |

| -- | -- | -- | + one share of stock |

| Synthetic Forward | t = 0 | t = 3 mo | t = 9 mo |

| Borrow | +S0 | -- | -FV9(S0) |

| Buy one share | -S0 | -- | + one share |

| Dividend | -- | D3mo | +FV9(D3mo) |

The equality of the cash flows requires:

Equation 2.1. - F(0,9) = - FV9(S0) + FV9(D3mo)

Since

FV9(D3mo) = PV0(D3mo) · (1+r9mo)9/12

and

FV9(S0) = S0 · (1 + r9mo)9/12

⇒ Equation 2.1. yields:

F(0,9) = FV9(S0) - FV9(D3mo) = {S0 - PV0(D3mo)} · (1 + r9mo)9/12

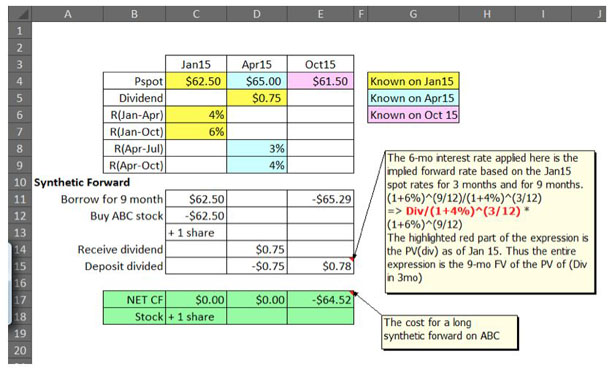

Example 2.6. (Forward Price on Assets with Known Income):

On January 15th, ABC stock is priced at $62.50 and will pay a $0.75 dividend in April 15th. The 3-month interest rate is 4%, the 9-month interest rate 6%, and the 12-month rate 7%.

- What would be an equilibrium price of a forward contract on the stock expiring on October 15th?

- What would be the value of a long forward contract above on April 15th, ex dividend? The stock price is $65.00, and the 3-month interest rate 3%, the 6-month rate 4%, and 9-month rate 5%.

- On October 15th, the expiration date, the stock price is $61.50. What is the value of the forward contract?

Click on Example 2.6. Solution to view the solution.

STEPS - using the discrete compounding method:

- Consider a synthetic forward: Buy ABC stock at the spot price with borrowed money for 9 months:

On January 15:

CF1/15 = + 62.50 (loan) – 62.50 (pay for stock) = 0

+ 1 share of ABC stock

+ a forward contract to deposit $0.75 on 4/15 for 6 months

[implied forward rate (1 + r9-mo)9/12/(1 + r3-mo)3/12]

On April 15:

+ $0.75 dividend

- $0.75 [deposit dividend at (1 + r9-mo)9/12/(1 + r3-mo)3/12 ]

CF4/15 = 0

On October 15

CF10/15 = - 62.50 · (1 + r9-mo)9/12(← loan repayment)

+ 0.75 · (1 + r9 - mo)9/12/(1 + r3 - mo)3/12 (← FV of div)⇒ Since the cash flows on January 15 & April 15 are both ZERO, the forward price should be equal to the cash flow on October 15 from the synthetic forward, CF10/15:

F(Jan 15, Oct 15) = FV10/15(S1/15 - PV1/15(Div4/15))

= (1+6%)(9/12){62.50 - 0.75/(1+4%)(3/12)} = $64.52

- The value of the long forward contract on April 15th is:

(Spot Price on Apr 15) minus PV of F(Jan 15, Oct 15) on Apr 15

= 65 - 64.52/(1 + 4%)(6/12) = 65 - 63.27 = 1.73

- The value the long forward contract on October 15th is:

(Spot Price on Oct 15) minus PV of F(Jan 15, Oct 15) on Oct 15

= 61.50 - 64.52 = - 3.02The figure below is an Excel Worksheet solving this problem:

Figure 2.6. Example 2.6. Solution Excel File