Main Content

Lesson 3 The Economics of Higher Education Institutions

Institutional Expenditures

Describing where colleges get their money is much easier than describing how colleges spend their money. Higher education institutions jointly produce a lot of different items as they educate students, conduct research, and perform public service, with each of these activities requiring a lot of different tasks. For example, the education of students requires direct instruction, out-of-class learning opportunities, advising, counseling, student conduct hearings, financial aid assistance, orientation, and a variety of other tasks.

To describe spending, you need to assign specific costs to specific activities, and because most of the costs of colleges reflect salaries to employees, you essentially need to assign people to specific activities. That task, however, is not always straightforward. For example, the full-time faculty in the higher education program engage in research, instruction, advising, recruitment, admissions, general administration, and public service. What percentage of each faculty member’s salary should be assigned to each of these tasks? No clear answers exist to this question, so colleges and universities are forced to make arbitrary assumptions when assigning personnel costs to activities. When you examine differences across colleges and universities in how much they spend on certain activities, part of the differences across schools reflect differences in the assumptions that schools make when assigning personnel costs to activities. Consequently, one is never sure whether the differences across schools reflect real differences in how they operate or reflect differences in how they calculate their costs.

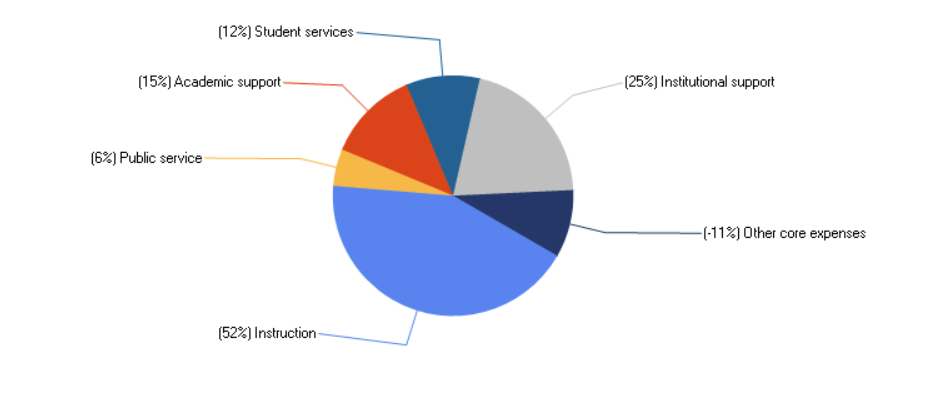

Complicating the analysis is that the true differences across higher education institutions in their spending patterns is not that large. As you can see from the below expenditure figures, the not-for-profit institutions vary little in their spending patterns. Several of the differences that do exist likely reflect true differences in how the schools operate. For example, the figures reveal that the two research universities, Harvard and Purdue, spend around 20% on research while the other institutions spend very little. The figures also reveal that the the public institutions spend more on public service than the private institutions. Other differences, however, may simply reflect differences in accounting patterns. This latter explanation may explain some of the differences across schools in academic support, institutional support, and student services.

For-profit universities use different accounting rules, so the listed categories for for-profit schools aggregate across multiple categories that were used for the not-for-profits. The most striking finding for University of Phoenix is that only 19% of expenditures were on instruction, which likely reflects lower salaries paid to instructors and greater dollars spent on advertising. Not all for-profits, however, spend to the same degree on advertising, so the results observed for the University of Phoenix may not hold for all for-profits.

Figure 3.7 - Expenditure Profile, Harvard University, Source: IPEDS (U.S. Department of Education. Institute of Education Sciences, National Center for Education Statistics.)

Figure 3.8 - Expenditure Profile, Purdue University, Source: IPEDS (U.S. Department of Education. Institute of Education Sciences, National Center for Education Statistics.)

Figure 3.9 - Expenditure Profile, Bethel University, Source: IPEDS (U.S. Department of Education. Institute of Education Sciences, National Center for Education Statistics.)

Figure 3.10 - Expenditure Profile, Eastern Michigan University, Source: IPEDS (U.S. Department of Education. Institute of Education Sciences, National Center for Education Statistics.)

Figure 3.11 - Expenditure Profile, Cuyahoga, Source: IPEDS (U.S. Department of Education. Institute of Education Sciences, National Center for Education Statistics.)

Figure 3.12 - Expenditure Profile, University of Phoenix, Source: IPEDS (U.S. Department of Education. Institute of Education Sciences, National Center for Education Statistics.)

Definitions for Expenditure Categories

- Instruction: Activities directly related to instruction, including faculty salaries and benefits, office supplies, administration of academic departments, and the proportion of faculty salaries not going to departmental research and public service.

- Research: Sponsored or organized research, including research centers and project research. These costs are typically budgeted separately from other institutional spending, through special revenues restricted to these purposes.

- Public service: Activities established to provide noninstructional services to external groups. These costs are also budgeted separately, and include conferences, reference bureaus, cooperative extension services and public broadcasting.

- Student services: Noninstructional, student-related activities such as admissions, registrar services, career counseling, financial aid administration, student organizations and intramural athletics. Costs of recruitment, for instance, are typically embedded within student services.

- Academic support: Activities that support instruction, research, and public service. These include libraries, academic computing, museums, central academic administration (deans’ offices), and central personnel for curriculum and course development.

- Institutional support: General administrative services, executive management, legal and fiscal operations, public relations and central operations for physical plant operation.

![]()