MBADM811:

Lesson 1: Introduction to Financial Statements

Lesson 1 Overview

We're all familiar with many types of businesses: service businesses, such as attorney firms; retail businesses, such as department stores; manufacturing businesses, such as automakers; and financial businesses, such as credit card companies. Many companies combine activities—for example, providing services as well as making or selling products—as restaurants and beauty salons do. There is enormous variety in company activities. But one thing all types of businesses have in common is an accounting system: a consistent way to keep track of financial transactions and report the company’s financial condition to those who use this information.

The accounting system that U.S. companies typically use is based on Generally Accepted Accounting Principles, or GAAP, which have evolved over time—many centuries, in fact. GAAP does not dictate the exact accounting procedure for every business activity but rather provides guidelines for company managers to use in tracking financial information. The common business transactions covered in this course are accounted for in a standard way, and a company’s financial information is collected and reported on four standard financial statements: the balance sheet, the income statement, the statement of changes in stockholders’ (owners’) equity, and the statement of cash flows.

In this lesson, you will consider the types of financial information generated by a business and who uses that information. You will also be introduced to GAAP guidance and the conceptual framework underlying financial reporting. In addition, you will become familiar with the four basic financial statements and the information reported on each.

Learning Objectives

After completing this lesson, you should be able to do the following:

- Identify the internal and external stakeholders who are interested in a company’s financial information.

- Identify the general characteristics of financial information reported in accordance with GAAP, as outlined in the FASB’s conceptual framework.

- Name the four basic financial statements, and discuss the elements contained in each.

- Calculate retained earnings, and demonstrate how it relates to stockholders’ equity.

- Create a balance sheet, income statement, and statement of stockholders’ equity, given basic company financial data.

Lesson Readings and Activities

By the end of this lesson, make sure you have completed the readings and activities found in the Course Schedule.

Financial Information

Many pages in this lesson, and throughout the course, will instruct you to read certain pages from your textbook. The readings will be applicable to the lesson page on which they appear. In this lesson, the concepts from the textbook will be applied to a simple fictional business.

We will use a retail company as an example: Robyn's Retail, Inc. organized as a corporation. When establishing a company, owners choose one of several types. For a discussion of different types of company organization, see Chapter Supplement A on pages 23–24 of your text. The basics of the accounting system are the same for all types of companies, but some of the terminology and specific accounting practices might vary from one type of company to another. In this course, we will focus on corporations. The owners of corporations are called stockholders or shareholders.

Stockholders invested $50,000 for shares of common stock of Robyn's Retail, Inc. She began the business on September 1, 20xx. Robyn used some of the $50,000 to set up a small office and retail store in a rented space.

Think about the financial information Robyn's Retail will generate as it begins operations:

- Stockholders invested $50,000, which created an increase in cash and an increase in stockholders’ equity for that amount.

- Part of that cash was used to purchase supplies and equipment as well as pay in advance for rent and insurance.

- Robyn’s Retail purchased land for future business expansion by borrowing $20,000 from the bank. Interest will need to be paid periodically on this note payable.

- Inventory was purchased from suppliers who expect payment within a specific time period.

- Robyn’s Retail will use advertising to capture new customers.

- Sales will be collected in cash or billed on account.

Users of Financial Information

Now think about the stakeholders of Robyn's Retail—those who are interested in the company’s financial information.

Owners

Obviously, the stockholders are interested as the owners. They've invested in the company and expect a return on their investment. In other words, they expect that their initial share price will grow and that the company may pay dividends.

Managers

Managers are interested in financial information in their roles as managers of the business:

- Are the prices competitive with other retailers?

- What are their highest costs?

- How much does the company owe to suppliers?

- Are they getting paid promptly?

- Who still owes the company money?

- Are they making a profit?

The formal record-keeping process also provides control over financial information and assets:

- Utilizing a bank account provides third-party verification of deposits and withdrawals.

- Making prompt deposits safeguards cash received from customers.

- Reconciling the bank statement with purchase receipts helps prevent errors and would uncover any nonbusiness use of funds.

- Documentation helps ensure accuracy in billing and collecting from customers.

- When managers are responsible for these control activities, they're accountable to owners and other stakeholders and less likely to be tempted to commit fraud.

Creditors

Banks loan companies money. Investors buy corporate notes and bonds when issued by companies. These parties are creditors and are interested in whether the company is earning a profit and will be able to pay interest and principal on debt.

Government Entities

Companies hope to generate income as they conduct business, and the income may be taxed at the federal, state, and local levels. So government entities are also interested in collecting the financial information they need to levy taxes.

Internal Users

As you can see, owners, managers, creditors, and governments have different reasons for needing financial information. Managers are internal users of financial information. They typically need more detailed information pertaining to the day-to-day operations of the business in order to make managerial decisions about issues such as pricing, strategies to keep costs low, and how to encourage customers to pay promptly. The financial reports utilized by internal users are specific to the business and may be in any form beneficial for management use.

External Users

Owners, creditors, and governments are external users of financial information. In many companies, the owners are not involved in managing the business. For example, in public companies—those that have sold shares of ownership that can be traded in financial markets—the owners are investors that may keep their ownership rights for a limited period of time. They're interested in higher level, less detailed information, including periodic profits, how the corporate resources are invested, the level of debt, and how cash is generated. Creditors and governments, too, need a more general idea of the company’s financial health. Creditors are interested in its ability to repay loans, while governments need limited detail concerning taxable income. Other external users include employees, labor unions, and major customers and suppliers.

| Internal | External | |

|---|---|---|

| User |

|

|

| How information is used | Use detailed financial information to run the business, reported in any convenient format | Use summarized financial information reported in the financial statements |

Four basic financial reports are utilized by most external users:

- the balance sheet,

- income statement,

- statement of changes in stockholders’ equity, and

- statement of cash flows.

They're presented in a standardized format and, for public companies, must conform to GAAP guidelines. They provide a means for management to communicate the company’s financial information to outsiders. In addition, governments provide their own forms for managers to utilize in reporting the company’s taxable income. The focus in this course is on the communication provided by the four basic financial statements. A fifth report—the statement of comprehensive income—will be introduced later in the course.

Lesson 1 Exercise: Financial Statement Users

Practice Exercise

After reviewing the content on the previous page, please answer the questions provided. You have as many attempts as you need to correctly complete this exercise. You may also go back after receiving your point to use the exercise for additional practice.

GAAP Guidelines and Financial Reporting Standards

The financial statements are management’s communication to external users. Since management has knowledge of the company’s day-to-day transactions and external users do not, there's an inherent risk that management’s communication may be inaccurate, misleading, or presented in a way that makes it difficult for external users to compare the company’s financial condition to that of other companies. For this reason, standard-setting organizations provide standards and guidelines for management to follow in their accounting system and financial statement presentation. In the United States, the primary authority for accounting standards is the Securities and Exchange Commission (SEC), a government body. The SEC has the power to ensure that accounting standards are upheld and that financial statement users’ interests are protected. However, the SEC delegates responsibility for setting specific accounting standards to the Financial Accounting Standards Board (FASB), made up of accounting and finance experts with backgrounds in industry, auditing, education, and investing.

Remember that GAAP stands for Generally Accepted Accounting Principles, and some of these accounting principles have been in use for centuries. The FASB has created formal written descriptions of already-existing GAAP and has organized the guidance by topic into a framework called Codification. New guidance and revisions to old guidance are added to the Codification after a period of public comment and deliberations.

The FASB has also created a conceptual framework describing (1) the characteristics of useful accounting information, (2) the elements comprising the financial statements, and (3) assumptions and principles used throughout the accounting system. Here, we’ll consider the important characteristics of accounting information, as defined in the conceptual framework:

- Relevance: The information should help financial statement users confirm their assessment of the company’s financial condition, as well as predict the company’s financial future. Also, the information reported should be material—large enough or important enough to influence the decisions of a financial statement user.

- Faithful representation: The information should be complete, error-free, and neutral (unbiased).

- Enhancing characteristics: The information should be consistent (to allow for comparisons), verifiable, timely, and understandable.

In the following sections, we will look at the four financial statements, highlighting their elements and structure. Throughout the rest of the course, some of the assumptions and principles in the conceptual framework will be covered.

Lesson 1 Exercise: Conceptual Framework

Practice Exercise

After reviewing the content on the previous page, please answer the questions provided. You have as many attempts as you need to correctly complete this exercise. You may also go back after receiving your point to use the exercise for additional practice.

The Balance Sheet | Video

Robyn's Retail is a legal entity separate and apart from its owners. Once the owners invested $50,000, the money becomes a resource, or capital, and will be used by the company. Likewise, it's the company that will earn money using its resources. The financial information gathered and summarized for a company has the characteristics outlined in the FASB conceptual framework and can be summarized and presented using the four basic financial statements. First, we will consider the balance sheet.

The balance sheet contains information about a company’s financial position at a point in time—often the end of a year, quarter, or month. It's divided into three major sections, representing three of the elements in the conceptual framework:

- Assets: Probable future economic benefits owned by the entity as a result of past transactions. After the initial investment and purchases, Robyn's has cash, accounts receivable, inventory, prepaid rent, prepaid insurance, supplies, land, furniture and fixtures, and equipment. These assets represent resources that will benefit the company in the future.

- Liabilities: Probable future sacrifices of economic benefits arising from a present obligation to transfer cash, goods, or services as a result of a past transaction. Robyn's has obligation to pay suppliers reflected in accounts payable and the bank, in the long-term notes payable.

- Equity: The financing provided by owners and operations of the business. Owners provided $50,000 of financing or contributed capital, and Robyn's generated income in September of $1,292 retained in the business. We will see this in the income statement presented in the next section.

| Robyn's Retail | ||||

| Balance Sheet | ||||

| September 30, 20xx | ||||

| Current Assets | Current Liabilities | |||

| Cash | $ 28,150 | Accounts Payable | $ 5,250 | |

| Accounts Receivable | 800 | Unearned Revenue | 100 | |

| Inventory | 10,000 | Interest Payable | 50 | |

| Prepaid Rent | 8,800 | Total Current Liabs. | 5,400 | |

| Prepaid Insurance | 550 | |||

| Supplies | 500 | Long-Term Liabs. | ||

| Total Current Assets | 48,800 | Note Payable | 20,000 | |

| Non-Current Assets | Total LT Liabs. | 20,000 | ||

| Land | 20,000 | Total Liabilities | 25,400 | |

| Furniture & Fixtures | 3,000 | |||

| Equipment | 5,000 | Stockholders' Equity | ||

| Accum. Depreciation | (108) | Common Stock | 50,000 | |

| Net PP&E | 27,892 | Retained Earnings | 1,292 | |

| Total SE | 51,292 | |||

| Total Assets | $ 76,692 | Total Liabs. & SE | $ 76,692 | |

Please watch to learn more about the balance sheet for Robyn's Retail.

In the balance sheet, assets must always balance with, or equal, liabilities and equity. The relationship can be written as an equation (Figure 1.1).

This relationship is called the accounting equation. Later, you will learn how the accounting system records transactions to always keep the accounting equation—and the balance sheet—in balance. For now, it's important to be able to identify specific business items as assets, liabilities, or equity items. Select Next at the bottom of the page for a practice exercise.

Lesson 1 Exercise: Balance Sheet Items

Practice Exercise

After reviewing the content on the previous page, please answer the questions provided. You have as many attempts as you need to correctly complete this exercise. You may also go back after receiving your point to use the exercise for additional practice.

The Income Statement | Video

The income statement reports the operating results of the company for one period, such as a year, quarter, or month. A simple single-step income statement contains just two major elements:

- Revenues: amounts earned from selling goods or services during the period.

- Expenses: amounts incurred to generate revenues during the period.

A multiple-step income statement has multiple subtotals, like gross margin, operating income, and income before taxes. The excess of revenues over expenses is the company's net income. Net income is a measure of profit (or loss) for the period, so the income statement is sometimes referred to as a profit and loss (P&L) statement.

| Robyn's Retail | |||

| Income Statement | |||

| For the month ended September 30, 20xx | |||

| Sales revenue | $ 8,000 | ||

| Cost of Goods Sold | 5,000 | ||

| Gross Margin | 3,000 | ||

| Advertising expense | 250 | ||

| Utilities expense | 450 | ||

| Rent expense | 800 | ||

| Insurance expense | 50 | ||

| Depreciation expense | 108 | ||

| Total Operating expenses | 1,658 | ||

| Operating Income | 1,342 | ||

| Interest expense | 50 | ||

| Net Income | $ 1,292 | ||

Please watch to learn more about income statements.

Lesson 1 Exercise: Income Statement

Practice Exercise

After reviewing the content on the previous page, please answer the questions provided. You have as many attempts as you need to correctly complete this exercise. You may also go back after receiving your point to use the exercise for additional practice.

The Statement of Changes in Stockholders’ Equity | Video

The statement of changes in stockholders’ equity, as the name implies, reports any changes that have occurred in the components of equity. Often, it is called the statement of owners’ equity, or statement of stockholders’ equity if the company is a corporation. Three elements of FASB’s conceptual framework are found in this financial statement:

- Investments by owners: Transfers, usually cash, from owners to the company. Owners invested $50,000 in Robyn's Retail, which we have called common stock. Owners' investments increase contributed capital, which is part of equity, though not explicitly labeled as such. Common stock is contributed capital.

- Net income: Amounts generated through transactions with nonowners. In our discussion of the income statement, we saw that Robyn's Retail had transactions with customers to earn revenue, and with suppliers to purchase various items, resulting in net income of $1,292. Net income is an addition to equity each period. If there were a net loss, it would decrease equity.

- Distributions to owners: Transfers, usually cash, from the company to its owners. Cash dividends are distributions to owners, and these distributions decrease equity.

The accumulation of net income over the years, minus any distributions to owners, is called retained earnings. A statement of stockholders' equity shows changes in retained earnings by adding net income and subtracting dividends.

| Robyn's Retail | |||

| Statement of Shareholders' Equity | |||

| For the month ended September 30, 20xx | |||

| Common Stock | Retained Earnings | Total SE | |

| September 1, 20XX | $ - | $ - | $ - |

| Contribution by Owners | 50,000 | 50,000 | |

| Net Income | 1,292 | 1,292 | |

| Dividends | 0 | 0 | |

| September 30, 20XX | $ 50,000 | $ 1,292 | $ 51,292 |

Please watch to learn more about the statement of changes in owners' equity.

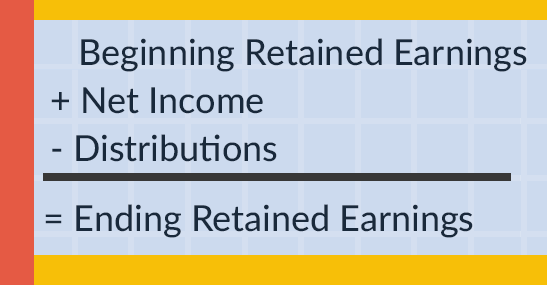

As noted, changes in retained earnings are shown in the statement of owners' equity. It is important to highlight the formula for retained earnings (Figure 1.2):

In a corporation, distributions to owners (stockholders) are called dividends. Always remember that distributions (dividends) are not reported in net income. In other words, distributions are not an expense and are not subtracted from revenues to arrive at net income. Rather, dividends are a direct reduction from retained earnings; they never pass through net income.

Lesson 1 Exercise: Retained Earnings

Practice Exercise

After reviewing the content on the previous page, please answer the questions provided. You have as many attempts as you need to correctly complete this exercise. You may also go back after receiving your point to use the exercise for additional practice.

The Statement of Cash Flows | Video

The statement of cash flows explains the change in cash from the beginning of the year to the end of the year. The statement reflects three types of business activities where cash is provided or used:

- Operating activities consist of the daily activities of the company related to earning income. However, revenues and expenses as reported on the income statement reflect cash and accrual elements. One method of creating the operating activities section of the cash flow statement alters net income to arrive at the net cash inflows or outflows from operations.

- Investing activities are transactions related to buying and selling long-term assets, such as property, plant, and equipment (PPE), or investments in securities, such as stocks and bonds.

- Financing activities include borrowing or paying off the principal amount of a loan, receiving capital contributions from owners, and paying cash distributions to owners.

This is a basic introduction to the statement of cash flows, and we will cover this topic in greater detail in Lesson 13.

Robyn’s statement of cash flows for the month of September would look like Table 1.5.

| Robyn's Retail | |||

| Statement of Cash Flows | |||

| For the month ended September 30, 20xx | |||

| Operating | |||

| Net Income | $ 1,292 | ||

| Depr. Exp | 108 | ||

| Inc. A/R | (800) | ||

| Inc. Inventory | (10,000) | ||

| Inc. PPD. Rent | (8,800) | ||

| Inc. PPD. Insurance | (550) | ||

| Inc. Supplies | (500) | ||

| Inc. A/P | 5,250 | ||

| Inc. Int. Payable | 50 | ||

| Inc. Unearned Revenue | 100 | ||

| Cash outflows from Operations | (13,850) | ||

| Investing | |||

| Purchase of Furn. & Fixtures | (3,000) | ||

| Purchase of Equipment | (5,000) | ||

| Cash outflows from investing | (8,000) | ||

| Financing | |||

| Issued Common Stock | 50,000 | ||

| Cash inflows from Financing | 50,000 | ||

| Net increase in cash | 28,150 | ||

| Beginning Cash | 0 | ||

| Ending Cash | $ 28,150 | ||

Please watch to learn more about the statement of cash flows.

Lesson 1 Exercise: Cash Flow Statement

Practice Exercise

After reviewing the content on the previous page, please answer the questions provided. You have as many attempts as you need to correctly complete this exercise. You may also go back after receiving your point to use the exercise for additional practice.

Relationships Among the Financial Statements

The information on the financial statements all comes from the same accounting system, and the four basic financial statements are all related to one another. Recall that the income statement calculates net income for the accounting period (usually a month, quarter, or year). The same net income is shown on the statement of stockholders’ equity, in the calculation of retained earnings for the period. Robyn's Retail's September net income of $1,292 is added to retained earnings in the September statement of stockholders’ equity. Total retained earnings and total owners’ equity are then shown on the balance sheet.

Figure 1.3 The Relationship Among Financial Statements for Robyn's Retail

Print Flowchart

First click on image to enlarge (image opens in a new window) then, from the new window, select Ctrl-P or CMD-P to use your browser's print function to print the image.

Figure 1.3 shows the relationship among financial statements for Robyn's Retail. Net income was calculated first because that carries over to the next statement, which is the statement of changes in stockholder's equity. On the statement of changes in stockholders' equity, retained earnings is calculated using the formula presented in Figure 1.2 (Beginning Retained Earnings + Net Income - Dividends = Ending Retained Earning). The retained earning amount can be seen on the balance sheet in the stockholders' equity section. Furthermore, the cash account on the balance sheet shows a balance of $28,150, which matches the bottom line of the statement of cash flows.

The Income, Stockholders' Equity, and the Balance Sheet

The relationships among the income statement, stockholders’ equity statement, and the balance sheet are summarized in Figure 1.3.

Details of operating revenues and expenses are shown on the income statement and summarized in net income. Net income carries over to the statement of stockholders' equity in the calculation of retained earnings. The final balance in retained earnings then carries over to the balance sheet, along with the balances of other equity accounts.

In addition, the reconciliation of cash in the statement of cash flows agrees with the balance in the cash account on the balance sheet. The four financial statements will always tie together in this manner. Another illustration of the financial statement relationships is shown on page 13 of your textbook.

The financial statements alone don't present enough information to enable investors and creditors to make informed decisions because they're presented in a summary format. They don't contain any information about the characteristics of the company, its choices of accounting methods, or details of complex transactions. For this reason, companies also present notes to the financial statements to provide a more complete communication of financial data. FASB guidelines strive to ensure that companies provide transparency in their financial statements, meaning that they do not hide or disguise information, which might mislead the users of the financial statements. In this course, we will sometimes refer to the financial statement notes and their contents when covering certain topics.

Lesson Summary

You are now familiar with types of financial information generated by a company and the stakeholders who are interested in that information: internal parties, such as managers, and external parties, such as owners and creditors. You've also learned about the elements and basic structure of four financial statements: the balance sheet, income statement, statement of changes in owners’ equity, and statement of cash flows, which comprise management’s communication to the public about the company’s financial condition. In the next lesson, you will learn how financial information is recorded in the company’s accounting system.

Lesson 1 Activities

Lesson 1 Zoom Session—Financial Statements

These live sessions are not required but are intended as supplemental learning experiences that delve deeper into each lesson. If you choose not to attend a live session, you should watch the recording at your convenience.

All synchronous sessions will be recorded for later viewing. To view recordings, select Media Gallery in the navigation menu.

To join the synchronous session, select Zoom in the course navigation window, and select "Join" for this session. Details and support are available in the Zoom Video Conferencing module.

Lesson 1 Discussion: Introduction (Single post due Sunday by 11:59 p.m. (ET)

No AI Use

AI Use Guidance

![]() You may not use any GenAI assistance to complete any part of this assignment.

You may not use any GenAI assistance to complete any part of this assignment.

See Key to AI Use for more information.

Please use this discussion board to introduce yourself to the class. Since this course is entirely online, it is a nice area to get to know your classmates or team project members.

For your initial post, do the following:

- Provide a brief summary of details you feel comfortable sharing, such as where you live, where you work, job role, and so on.

- MBA programs often require one or more Accounting courses. How do you see fundamental accounting knowledge benefitting your career goals?

- Please offer an additional interesting fact. Examples of this are “I speak five languages" or "I have 15 first cousins” or why you decided to return to school.

You may respond to another student’s post if you wish, although for this discussion it is not required.

Note: For some discussions in this course, there are two posts required. If there are two posts, the initial post is due by Thursday, 11:59 p.m. (ET) of the lesson week, and it is your thoughts based on the discussion prompt. The second post is due by the end of the lesson week (Sunday, 11:59 p.m. ET), and it is a reply to at least one other student’s post. A quirk within Canvas only allows the listing of one due date and the Sunday date is shown, so please make note of the earlier (Thursday) requirement for future discussions.

Posts should be 100–250 words in length. If you use any outside source for your posts, please include citations. Please see the rubric for the grading breakdown and the Syllabus for instructions about late posts.

Key to AI Use

Icons related to the use of generative artificial intelligence (GenAI) technologies, such as ChatGPT and Copilot, are used in the course. If GenAI is allowed in the course, each assignment should have an AI policy that will indicate how you may use GenAI, along with guidance on usage, ethics, and how to cite your use. Ask your course instructor or TA if you have questions.

Where to Find the Assignment AI Policy

First, look for the Assignment AI Policy at the top of your assignment and select the box to show the details. Select the box again to hide the details. Your assignment will have one of the following AI policies and should include details like which types of GenAI you may use, the purposes you may use them for, citation requirements, and other details. The following represent examples of AI Assignment Policies and details.

Limited AI Use

-

AI Use Guidance

You may use minimal GenAI assistance for the following purpose:

") to check spelling and grammar

to check spelling and grammar -

Citations

Acknowledge the type of GenAI used.

-

Ethical AI Use Reminder

Across all levels of GenAI use, you should consider ethical implications, which includes using a safe, secure, humane, transparent, and environmentally friendly approach to GenAI.

See Key to AI Use for more information.

Assignment AI Policy

Your assignment will have one of the following GenAI assignment policies, along with details. If you don't find an AI Assignment Policy, assume that you cannot use GenAI. Ask your course instructor or TA if you have any questions.

No AI Use

No AI Use Example

![]() You may not use any GenAI assistance to complete any part of this assignment.

You may not use any GenAI assistance to complete any part of this assignment.

As your instructor, I am most interested in your thoughts and reflections from traveling and how you express the integration of course concepts into your travel experiences. For this reason, no GenAI use is permitted in the completion of this assignment.

Limited AI Use

Limited AI Use Example

You may use minimal GenAI assistance for the following purpose:

![]() to check spelling and grammar

to check spelling and grammar

-

Citations

If you use GenAI tools for minimum assistance, add an acknowledgement statement that includes the type of GenAI used (e.g., I acknowledge that I have used [insert name of GenAI tool—Grammarly, Copilot] to edit my document for grammar and spelling.)

-

Ethical AI Use Reminder

Across all levels of GenAI use, you should consider ethical implications, which include using a safe, secure, humane, transparent, and environmentally friendly approach to GenAI.

Moderate AI Use

Moderate AI Use Example

You may use GenAI for moderate assistance, including the following:

idea generation and general brainstorming

idea generation and general brainstorming

![]() to assist with data analysis

to assist with data analysis

![]() to check spelling and grammar

to check spelling and grammar

-

Citations

Acknowledge the type of GenAI used. You may be asked to explain where and how GenAI was used in this assignment, as well as your contribution to the assignment.

-

Ethical AI Use Reminder

Across all levels of GenAI use, you should consider ethical implications, which include using a safe, secure, humane, transparent, and environmentally friendly approach to GenAI.

Full AI Use

Full AI Use Example

You may make full use of GenAI, including the following:

idea generation and general brainstorming

![]() to assist with data analysis

to assist with data analysis

![]() to check spelling and grammar

to check spelling and grammar

![]() to outline a paper or assignment

to outline a paper or assignment

![]() to generate the initial work product or first draft

to generate the initial work product or first draft

![]() to rewrite, edit, or polish

to rewrite, edit, or polish

![]() to generate images

to generate images

![]() to generate audio

to generate audio

![]() to generate video

to generate video

![]() This icon may be used alone or with other icons to provide specific GenAI usage guidelines for an assignment.

This icon may be used alone or with other icons to provide specific GenAI usage guidelines for an assignment.

-

Citations

Acknowledge the type of GenAI used. You may be asked to explain where and how GenAI was used in this assignment, as well as your contribution to the assignment.

-

Ethical AI Use Reminder

Across all levels of GenAI use, you should consider ethical implications, which include using a safe, secure, humane, transparent, and environmentally friendly approach to GenAI.

Specific Assignment AI Expectations and Notes

This icon may be used alone or with other icons to provide specific GenAI usage guidelines for an assignment. Always check individual assignment instructions.

This icon may be used alone or with other icons to provide specific GenAI usage guidelines for an assignment. Always check individual assignment instructions.

![]() Modified from the AI Icon Project at Oregon State University. This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.

Modified from the AI Icon Project at Oregon State University. This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.