Main Content

Lesson 1: Course Expectations and Research

A Little Review Never Hurts!

It would be easy to assume that you are positively brilliant at the mechanics of accounting; the design and operation of an accounting system; and the proper application of generally accepted accounting principles GAAP. However, as auditors, we never assume.

Your first lesson in auditing begins with a review of financial accounting. We do this because the financial statements and the related disclosures are the focus of the financial statement audit. Financial accounting is the process responsible for the preparation of the financial statements and related disclosures.

There is another purpose to this particular lesson. Many of you will be graduating this semester. That means you will be going to interviews. Your potential employers will expect you to know this stuff. Our hope is that part of this lesson will help you feel better prepared, confident, and be very impressive when interviewing.

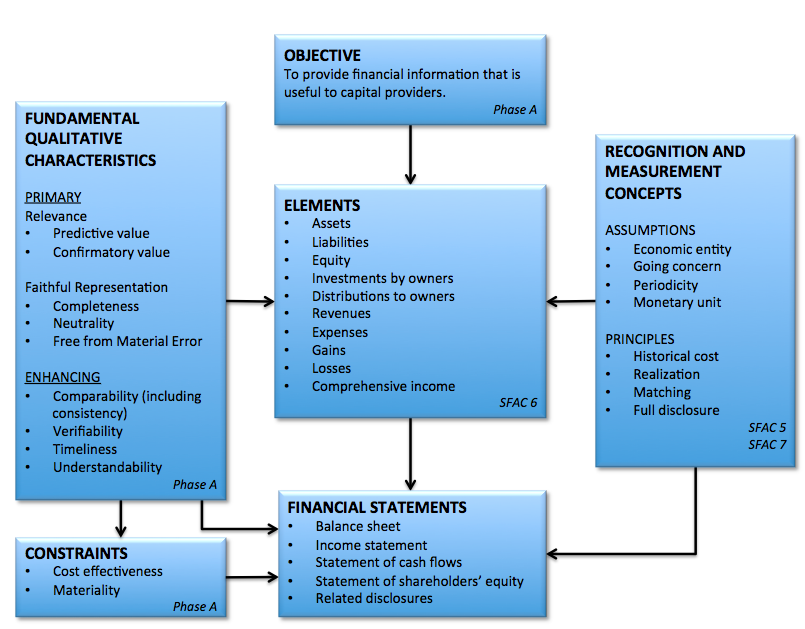

We refer to the financial statements and related disclosures throughout the course, so let's begin by visiting the GAAP based framework used for financial reporting, shown in Exhibit 1.

Exhibit 1: GAAP Framework

The size of the company does not matter. Whether the audit is performed on a Fortune 100 company or small business, the company is expected to prepare their financial statements using this framework. The audit process is designed to test for adherence to these GAAP concepts and promulgated standards. Failure to following the Historical Cost Principle is a departure from GAAP. The financial statements would not present fairly the results of operations, the income statement or financial position, or the balance sheet for the year.