Main Content

Lesson 1: Course Orientation and Defining Managerial Accounting

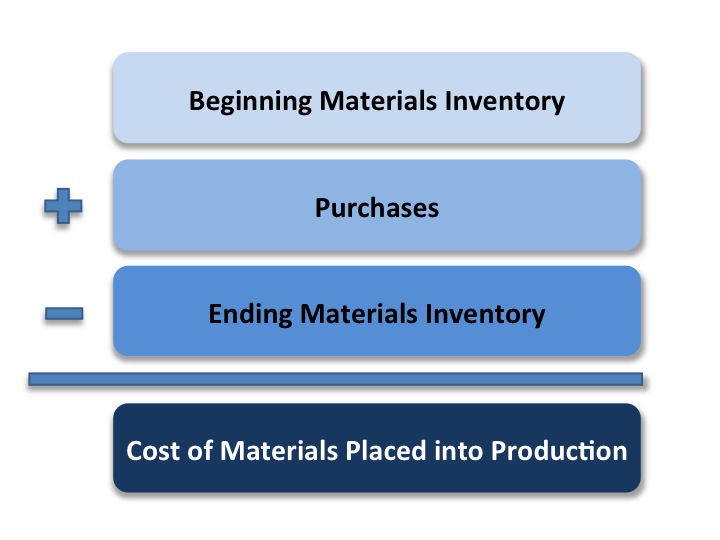

Step 1: Cost of Materials Placed into Production

The first step in determining COGS for a manufacturing company is to establish the cost of materials placed into production. This is the amount of materials the company takes from materials inventory and puts into production. The formula to calculate this is shown in Formula 1.1.

|

Guided Example

For your example, determining cost of materials placed into production would look like this:| Beginning Materials Inventory | $ 450,000 | |

| + | Purchases | + $ 750,000 |

| - | Ending Materials Inventory | - $ 420,000 |

| Cost of Goods Placed into Production | $ 780,000 | |